|

Holdovers A holding place for articles linked-to from within a subsequent newsletter article when the older newsletter is replaced every two weeks.

Dr. Gary North: Just Ignorant? Or Is There Something Else Going On? HAVE YOU EVER FELT PRESSURED TO PAY AN INCOME TAX you didn't really owe? Have you ever faced bad behavior from a government agency over an illegitimate tax charge-- be it an asserted "penalty" or alleged "deficiency" or even just a protracted delay in getting your legitimate refund? Blame folks like Gary North. To pick the most recent example of which I am aware, in his July 4 column this year, North declares: "Taxation has three main forms: direct (income, property, retail sales), indirect (wholesale sales), and monetary inflation." Is North just this ignorant? That's hard to imagine. Often he writes very cogently on many different subjects. So what's going on here? Here is the truth, as is known to any competent student of the subject (all emphases added): "[The] tax upon gains, profits, and income [is] an excise or duty, and not a direct tax, within the meaning of the constitution, and [] its imposition [is] not, therefore, unconstitutional." United States Supreme Court, Springer v. U. S., 102 U.S. 586 (1880) (as summarized in Pollock v. Farmer's Loan & Trust, 158 U.S. 601, (1895)) "[T]axation on income [is] in its nature an excise..." A unanimous United States Supreme Court in Brushaber v. Union Pacific R. Co., 240 U.S. 1 (1916) "I hereby certify that the following is a true and faithful statement of the gains, profits, or income of _____ _____, of the _____ of _____, in the county of _____, and State of _____, whether derived from any kind of property, rents, interest, dividends, salary, or from any profession, trade, employment, or vocation, or from any other source whatever, from the 1st day of January to the 31st day of December, 1862, both days inclusive, and subject to an income tax under the excise laws of the United States." The “affirmation” on the first income tax return form. "The income tax... ...is an excise tax with respect to certain activities and privileges which is measured by reference to the income which they produce. The income is not the subject of the tax; it is the basis for determining the amount of tax.” ... "[The Sixteenth] amendment made it possible to bring investment income within the scope of the general income-tax law, but did not change the character of the tax. It is still fundamentally an excise or duty with respect to the privilege of carrying on any activity or owning any property which produces income." Former Treasury Department legislative draftsman F. Morse Hubbard in testimony before Congress in 1943 "The [Sixteenth] Amendment, the [Supreme] court said, judged by the purpose for which it was passed, does not treat income taxes as direct taxes but simply removed the ground which led to their being considered as such in the Pollock case, namely, the source of the income. Therefore, they are again to be classified in the class of indirect taxes to which they by nature belong." Cornell Law Quarterly, 1 Cornell L. Q. 298 (1915-16) "In Brushaber v. Union Pacific Railroad Co., Mr. C. J. White, upholding the income tax imposed by the Tariff Act of 1913, construed the Amendment as a declaration that an income tax is "indirect," rather than as making an exception to the rule that direct taxes must be apportioned." Harvard Law Review, 29 Harv. L. Rev. 536 (1915-16) "If [a] tax is a direct one, it shall be apportioned according to the census or enumeration. If it is a duty, impost, or excise, it shall be uniform throughout the United States. Together, these classes include every form of tax appropriate to sovereignty. Whether the [income] tax is to be classified as an "excise" is in truth not of critical importance [for this analysis]. If not that, it is an "impost", or a "duty". A capitation or other "direct" tax it certainly is not." U.S. Supreme Court, Steward Machine Co. v. Collector of Internal Revenue, 301 U.S. 548 (1937) (citations omitted.) "The Supreme Court, in a decision written by Chief Justice White, first noted that the Sixteenth Amendment did not authorize any new type of tax, nor did it repeal or revoke the tax clauses of Article I of the Constitution, quoted above. Direct taxes were, notwithstanding the advent of the Sixteenth Amendment, still subject to the rule of apportionment…" Legislative Attorney of the American Law Division of the Library of Congress Howard M. Zaritsky in his 1979 Report No. 80-19A, entitled 'Some Constitutional Questions Regarding the Federal Income Tax Laws' SO, IN LIGHT OF THE FACTS, why is Gary North saying the income tax is a direct tax? I suppose I could be mistaken, but it seems to be that to declare the income tax to be a direct tax is a lie, in either of two forms: 1. You know better, and are deliberately mis-stating what you know, or 2. You have no idea what you're talking about, but are deceitfully implying that you do. Which one is it in this case? Dr. Gary North's integrity is his own problem in the most important sense, of course. But his words reach a lot of people. It is because of mis-statements like this from people like Gary North that anyone else is dealing with bad behavior by government actors. The myths about the tax are the cover under which the bad behavior avoids revealing and disinfecting sunlight, and they are also the intellectual undergrowth that keeps the liberating, bad-behavior suppressing truth about the tax from being ascendant and in charge. Every person who hears the lie that the income tax is a direct tax then has no reason to question its application to his or her own activities and the resultant gains. Mis-statements like North's keep juries and attorneys and even judges (most of whom know nothing independently about the tax in any broad sense) ignorant and dangerous to liberty and the rule of law. When it is understood that the tax is an excise (and what that means), suddenly everything else about it can start to come into focus (as, for instance, by following this simple chain of facts and logic). It is to avoid this onset of clarity that the beneficiaries of the tax scam do everything they can to promote the myth that it is a direct tax, with the critically-important help of shills like Gary North (and many others). I hope everyone can help (and help look out for all our interests) by 1. vigorously countering these injections of dis-information with rebuttals; 2. diligently inoculating the body politic with liberating truth; and 3. encouraging shills like Gary North to find something else to do. ***** What Are We? Serfs, Or Free Americans? Deploying simple logic against simple-minded lies... SO, HERE'S THE QUESTION: DO WE PAY TAXES BECAUSE WE OWE AN INHERENT DUTY TO THE STATE? That is, do Americans have tax obligations based in a subordinate status to the sovereign state, which by right can make us give it a portion of what we produce? Or, do Americans' tax obligations arise, if at all, because they have done something specific and defined, on the basis of which the obligation has arisen? It's either one of those ways or the other, you realize. There is no third alternative... Either you owe a tax because you've done something-- other than merely producing-- which is specified in law as taxable, is defined and is distinguished by qualifying facts (any allegation of which may or may not be true, and must be proven if disputed), or you owe it as a serf owes a percentage of whatever he produces to his lord-- just 'cause you're a serf and he's your lord, and if you produce something, he gets some of it. Turning this around, any assertion of a tax obligation (or of the conditions under which one could arise) which is effectively NOT vulnerable to challenge is a de facto enserfment. If a tax can be asserted-- even one nominally-based on qualifying facts-- and you can't freely dispute that those facts are true in any given case, then the tax is being applied as to a serf. "Freely dispute" necessarily embraces a dispute at the get-go. For example, in the case of the income tax, "freely dispute" would mean "free to dispute that "income" has been received". Since the tax falls on "income", unless one is free to declare that one has not received "income" (with that declaration given full and equal weight in the contest of allegations), one is not free to dispute anything meaningful at all. Unable to dispute the allegation at the get-go, you're left with nothing but asking for indulgence from your master. "Master, I've agreed that I did what allows you to claim ownership of my property by right, but I'd like to argue about how much of my stuff the law say you can take..." That's the whine of a serf. Rather different from the declaration of a free man or woman: "Hey, I didn't do anything giving you a claim to my stuff. If you think otherwise, prove it." Unless the income tax is actually a tax on the mere production of wealth, then, any harm or threat of harm leveled at a declaration on a 1040 that no "income" has been received, or effort to compel someone to declare that his or her earnings qualify as "income"-- such as by a "frivolous penalty", for instance, or any other kind of sanction-- is unlawful. Any disregard of a return because it declares no "income", or fails to declare received earnings to be "income", is equally unlawful. The income tax is NOT a tax on mere production, of course. It is, rather, an excise, as is acknowledged by every possible authority. Because this is so, it is clear, per the reasoning above, that anything having the appearance of a threat or discouragement to free dispute of the receipt of "income" is inherently frivolous and fictional, if not outright criminal. By the same token, it is clear that any notion of the tax as an involuntary imposition is misguided. There are two things, then, that come from this discussion. 1.) The legal minded or legally-engaged folks in the community should work on briefs deploying the logic above against those occasions when educated filings are responded-to with threats or disregard; and 2.) Everyone should work on those in the larger community who harbor the fictional notion that the tax is involuntary either as to its objects or its lawful administration. These folks need to be made clear on the fact that to the degree that the tax is administered as though involuntary, it is being administered contrary to its own statutory structure, and THAT'S the problem, not the tax itself. These folks also need to be made clear on the fact that this is why the state is so fixated on suppressing CtC-- the book exposes the process by which they and their children are being effectively enserfed; reveals that what is being done is actually contrary to the law; and explains what can and must be done to remain free in the face of this threat. "Although all men are born free, slavery has been the general lot of the human race. Ignorant--they have been cheated; asleep--they have been surprised; divided--the yoke has been forced upon them. But what is the lesson?…the people ought to be enlightened, to be awakened, to be united, that after establishing a government they should watch over it....It is universally admitted that a well-instructed people alone can be permanently free." -James Madison QUESTION FOR YOU ALL: Why am I the only one writing this article? Do you think that everyone else is going to suddenly "get it" and stop ruining your life with lies and misunderstandings of the tax, and stop trying to take half your hard-earned wealth, because of my feeble voice alone? ARE YOU CRAZY?! Every single one of you should be studying this material 'til you can recite it in your sleep, driving the deniers and distracters from within our ranks, and writing articles of your own and posting them everywhere you can, online and in print. ***** "That's Inconceivable!"- II Though the truth about the income tax may seem "inconceivable" to some, the events documented here would NEVER happen--NOT EVEN ONCE-- if CtC weren't completely correct. I'M PLEASED TO POST ANOTHER OF THE OCCASIONAL STANDOUTS among victories by CtC-educated Americans reclaiming their money and their independence from purveyors of the "income" tax scheme. These standouts are notable amongst the tens of thousands of other victories for having especially direct and deliberate tax agency involvement in their realization, thereby emphasizing the fact that what CtC has revealed about the tax is 100% accurate and 100% complete. This week's standout example is typical of these especially notable victories in enforcing the fundamental law. It offers plain and unambiguous documentation that before and while issuing the complete refund claimed by this CtC-educated American of EVERYTHING withheld or paid in to the United States in connection with the income tax-- Social Security and Medicare taps included-- the IRS was fully aware that this man:

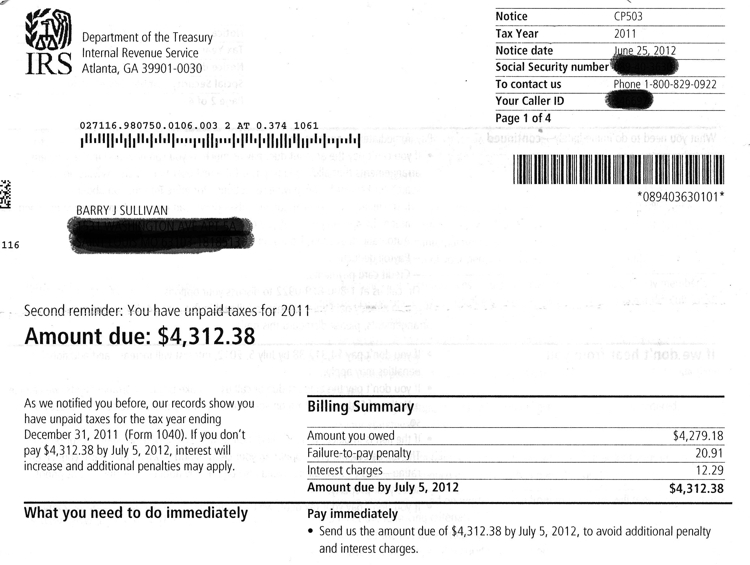

In other words, the IRS consciously, deliberately and explicitly agrees with the validity of this CtC-educated filer's reasoning and the specifics of his claim-- just as it has done in perhaps 200,000 or so other cases over the last ten-and-a-half years. HERE IS THIS LATEST OUTSTANDING EXAMPLE: Barry Sullivan filed a "conventional" original federal income tax return concerning 2011. This was done prior to Barry learning the actual and complete truth about the tax by reading 'Cracking the Code- The Fascinating Truth About Taxation In America', the book uniquely feared by corrupt government officials across the land, and the subject of a bizarre campaign to discourage reading of the book (while not banning it outright for fear of that being a step too far for even our seriously-compromised courts to stomach or that doing so would draw too much curious attention to it) even while filings and claims informed by the book's revelations are routinely and dutifully honored. When I say Barry filed a "conventional" return, I mean one reflecting belief in the 75-year-old government-encouraged myth that Barry's grandparents had inexplicably authorized the feds to charge all Americans a percentage of everything they earned, even when the feds had contributed nothing toward producing the gains. In other words, a return reflecting a belief that in 1913, Barry's grandparents and everyone else had decided to enslave themselves and their descendants. In the thrall of this absurd state-serving fairy tale, Barry had reported all the money that had come in to him during 2011 as "income"-- a $28,000 inheritance from what had been saved as a parent's IRA, and $15,550 that he had earned working. He followed the instructions on the form and ended up calculating a $4,364 tax liability on these amounts he had assumed were subject to the tax, and was reporting as such. Unfortunately, Barry didn't have the money and had only had $182 withheld from his pay as nominal "federal income tax". Crediting him nothing for the federal income tax pre-payments denominated as "Social Security and Medicare taxes", which Barry didn't know to claim in any event, just as he then didn't know to point out that he had no liability for the work-gains in connection with which those amounts were withheld, the IRS calculated an outstanding tax liability for Barry of $4,312.38 as of July 5, 2012:

Barry entered into a payment plan agreement, and started chunking out his hard-earned money to pay this amount. By February of 2014, he had paid the liability down to $2,910.54 (after additional accumulated penalty and interest amounts):

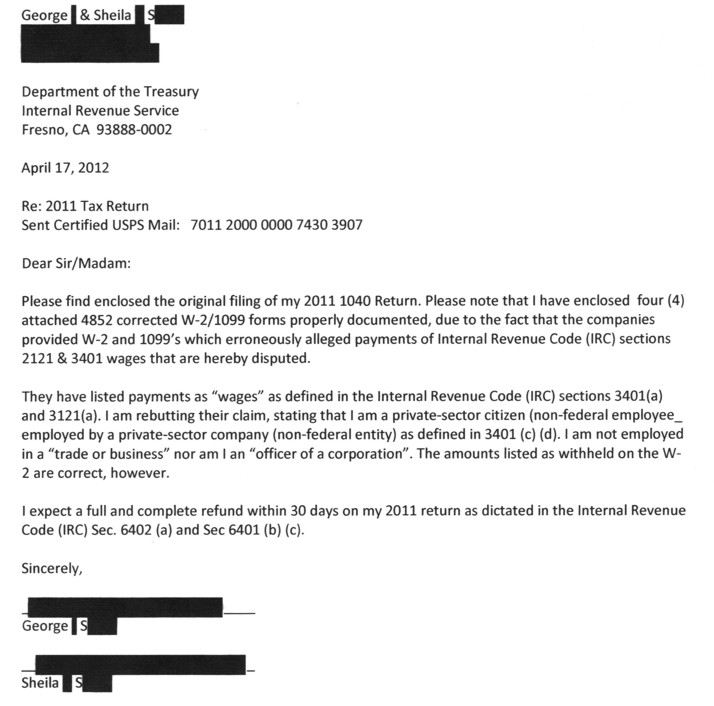

But then Barry threw in a game-changer. He had learned the truth about the tax, amongst which is the fact that the even when the law is on your side it does nothing on its own, and your inaction will be ruthlessly exploited by revenue-hungry tax agencies. Accordingly, Barry stood up, metaphorically, and straightened everything out. ON MARCH 1, 2014, RATHER THAN SEND IN THE $150 DEMANDED BY THE IRS, Barry instead sent in a 1040X amending his original "ignorance-tax" return. As you saw when you clicked on that link, Barry's amended return was accompanied by a cover letter explaining just what was being done (and that it was being done after consultation with the IRS about how to proceed), and a Form 4852 rebutting the erroneous allegations that his work was federally-connected which inhere in the use of a W-2 to report earnings, and which Barry had previously endorsed by attaching the W-2 to his original return and transcribing its numbers into the "wage" field on that 1040. Barry's Form 4852 also offered a detailed explanation of the reasoning on which his amendment was based.:

Barry calculated a new liability of only $1,851-- this being on only the IRA payout, which Barry treated as taxable on the amended filing. Against this was now the TOTAL amount of $1,060 withheld from Barry from his work-earnings, Social security and Medicare taxes included, plus what Barry had paid in installments. The result of Barry's amended filing was just what it should be and usually is without quibbling or complaint-- a prompt and complete agreement with all of his conclusions. Barry's tax liability is reduced by $2,513 due to his pay being entirely non-taxable, and his credit against the undisputed liability for the IRA funds he inherited going up $878-- every penny of what was withheld from him as Social security and Medicare taxes on that pay:

BY THE WAY, the same day Barry filed his amended return concerning 2011, he also filed his educated original return for 2013. This one contained not just a 4852 rebutting an erroneous W-2 but also two 1099 rebuttals. See that return package here. The result of this 2013 filing and claim? Just as with Barry's simultaneously-filed educated amendment, this filing concerning 2013 produced a prompt, complete agreement with Barry's conclusions and the refund of everything withheld (other than $3 due to an apparent typo-- $619.98 was withheld but it was transcribed to the 1040 as $616.98)-- all of which consisted of Social Security and Medicare withholdings:

Nice stand-up work, Barry! SO, HERE'S THE THING: I know that aloud or subconsciously, the "income tax Keynesians" out there are whispering in mind-numbing shock, "THAT'S INCONCEIVABLE!" Or, to put it more accurately, the Keynesians' little Stepford brains are busily trying to process these facts into something other than what they actually mean, because the prospect that they (the income tax Keynesians) are and have been so wrong about the tax all these years is INCONCEIVABLE!! I'm going to mercilessly lay it out, though, without regard to the risk of snapped synapses, and in an annoying "shout" because otherwise some folks just won't read, and I don't know what else to do: NOT ONE VICTORY LIKE BARRY SULLIVAN'S WOULD EVER HAPPEN-- NOT ONE-- IF CtC WERE NOT COMPELTELY CORRECT I know some folks have hung on troll-posts about the DOJ attacking my own filings a few years ago with "false return" charges (by which is ludicrously meant, "filing returns I did not actually believe to be true"), and on sporadic incidents of resistance to educated filings by the IRS-- news of which is constantly injected into circulation by the agency-- to convince themselves that CtC must be wrong, or at least incomplete. These conclusions are clung-to, of course, without any effort to actually read the details of these events so as to discover the dodges, evasions, and legal games played in both the civil and criminal assaults on me, and in the occasional efforts to resist educated filings. But even knowledge of what really goes on in these instances of negative reaction isn't needed to understand that efforts to resist or discourage are evidence of nothing. Even without looking at the damning details of these negative reactions, only a naif would imagine that government officials would never bring charges or attempt to discourage certain behavior unless actual crimes had been committed, or the behavior was actually wrong. Such reactions say nothing about the rightness or wrongness of CtC. BUT VICTORIES LIKE BARRY SULLIVAN'S SAY EVERYTHING. NO RATIONAL, GROWN-UP MIND CAN DENY THAT NOT ONE VICTORY LIKE BARRY SULLIVAN'S WOULD EVER HAPPEN-- NOT ONE-- IF CtC WERE NOT COMPLETELY CORRECT. SO STOP THE DAMNED DENIALS!! I don't care if the Keynesians (or anyone else who has been in denial) want to argue about the difficulties of acting on the truth about the tax, or about what will happen when that truth is widely acknowledged. Go for it, lads, and lasses! Write your columns and your scholarly papers; worry or celebrate as your commitment to liberty moves you. BUT NO MORE DENYING THAT TRUTH! Since the first 'Every Which Way But Loose' episode was posted, or even just the tenth, or hundredth, or five-hundreth historically-unprecedented refund complete with Social security and Medicare taxes included, denial has been a shameful self-deception and black lie of omission to the rest of the world. It has also been a great tragedy. What CtC reveals is the key to collapsing the state back to the dimensions and limitations intended by the Founders and Framers, and to which CtC-revealed knowledge had for the most part successfully confined it for 140 years: When writing CtC eleven years ago, I was all afire with the knowledge that I had actually belled the cat, gotten the emperor's new clothes-makers on tape admitting their scam, and charted a course by which America could get back to the limited republic it is meant to be. The limited republic by which Americans were safe, prosperous and free, and America was a shining beacon revealing the benefits of real human liberty to all the rest of the world. I knew that I simply needed to present what I had learned and the terrible and ruinous scourge of the mis-applied income tax would collapse back into its proper shape as an important but relatively modest little excise, recapturing for public benefit some of the private gains realized by the exercise of public privilege. All it would take is the word getting out there to enough people. That's still all it will take. Maybe Barry Sullivan's proof-of-the-pudding will finally crack the ice in the minds and throats of the deniers who have kept their voices from this effort. I hope so. Every day, the beneficiaries of the status quo work like beavers to figure out how to permanently evade the truth. They have now gone so far as to launch deadly, unprecedented attacks on the jury system in their ongoing effort to preserve their self-serving myths so thoroughly punctured by Barry Sullivan and all those other CtC-educated, activist Americans whose ranks Barry joins. (It's amazing how many never-before-in-American-history events have occurred in connection with CtC-- both positive and negative...) If the deniers DON'T get their thumbs out of their mouths, the chance might vanish, because the state may just descend all the way to the Full Monty in desperate defense of its "good thing". That'd be a heck of a price to pay just because certain folks find denial, even in the face of overwhelming evidence, easier than facing a truth they've convinced themselves is "inconceivable".

When an honest but mistaken man learns of his error, he either [forthrightly] ceases to be mistaken, or ceases to be honest.

"It is easier to fool people than to convince them that they have been fooled." -Mark Twain

***** Giving A Tax-Keynesian A Little Schooling FOLKS WHO STILL CLING TO STATIST MYTHOLOGY ABOUT THE INCOME TAX AND ASSOCIATED LAW are like Keynesians in the realm of economics. They are seemingly incapable of recognizing (or admitting) that they were wrong and that the Austrians are right, no matter how overwhelming the evidence. Kind of tragicomically, as much as they would vehemently protest against it, these stubborn statists are also adherents to the doctrine of "living law". After all, they take as authoritative of the scope of the tax merely what the current power structure would like everyone to believe it is. The "income tax Keynesians" embrace the latest power-preferred-belief despite the fact that it is contrary to what the tax laws actually say and contrary to what the courts have said about those laws. They embrace the latest power-preferred-belief even though it's contrary to what those who enacted both the relevant statutes and the Constitutional provisions to which they must conform plainly said they meant them to be. In fact, when obliged to do so by educated Americans, even the powers-that-be themselves acknowledge that the belief they want everyone to harbor about the tax is untrue, and that the tax remains just as it was written. But the Keynesians persist in arguing that the tax has been transformed into what the powers-that-be simply want people to believe about it. Like it or not, that's deeming the tax laws to be "living laws." I IMAGINE THE "INCOME TAX KEYNESIANS" BELIEVE the Fourth Amendment actually allows for warrantless seizure of everyone's papers and effects, anytime the state wants them. After all, it's what the state wants everyone to believe is true about the amendment's meaning. These Keynesians must also believe the Second Amendment doesn't reflect Constitutional respect for non-state-controlled citizen possession of weapons. After all, the state has long struggled mightily to get everyone to believe that the amendment only concerns some kind of state-regulated "group right". I SUPPOSE THESE "INCOME TAX" KEYNESIANS MUST STILL BE IN A SORT OF DENIAL/SHOCK MODE over the IRS having given everyone in the country a "rebate" on illegally collected "phone taxes" in 2007. After all, the state had been collecting them for decades, even over the sustained protest of many Americans. Those in power had vigorously and persistently encouraged everyone to believe that those phone taxes were valid. Even though the "phone tax" took in a mere pittance, and its misapplication relied entirely on a 8th-grade-education-obvious misconstruction of a single word ("and"), it was vigorously defended in court by the DOJ on behalf of the IRS for years. By the metric of the "income tax Keynesians", then, the "phone tax" MUST have been legal. What the law creating it actually says, or what those who enacted it meant it to be are irrelevant to its legitimacy. So when 6 out of 6 federal circuit courts finally admitted eight years ago that the decades-old "phone tax" application to most Americans had actually been CONTRARY to the real meaning and effect of the law all that time, the tax Keynesians must have in shock. They must have thought, "The tax had been being collected! The powers that be wanted us all to believe the tax applied as they were applying it! Why did these courts even LOOK at the words of the law itself? WE don't! After all, what do THEY matter?! The meaning of the law is whatever the current-powers-that-be have convinced everyone to believe that it is!"Sadly, the ill effects of that shock persist. Despite that nice object lesson, these Keynesians can't bring themselves to shine its light on the "income tax". Maybe it's because what the powers-that-be want everyone to believe about the "income tax"-- which DOESN'T bring in a "mere pittance", and is the #1 statist weapon against individual self-determination-- is SO much more vigorously defended than was the misapplied "phone tax". The ubiquitous, systemic character of the infectious defensive mythology deployed on behalf of state defiance of the truth about the income tax is so powerful as to drive even the obvious lesson of the "phone tax" out of the Keynesians' minds. ANYWAY, CtC-EDUCATED SCHOLAR GREG SUTTON has generously made an effort to shake one of the leading members of the "Keynesian school of tax pundits"-- Jacob Hornberger (founder and president of the Future of Freedom Foundation)-- out of his shocked state and into the sunlight. Greg's effort is prompted by Hornberger's recent "tax-day"-timed posts inanely calling for the abolition of the income tax based on taking the representations of the nature of the tax by the powers-that-be at face value (and bouncing off some ill-educated mid-Twentieth-Century writings on the subject by the otherwise usually very worthwhile essayist Frank Chodorov). Such abolitionist calls simply support and advance the statist mythology about the tax, and serve only to fasten its misapplication ever more tightly on everyone else. They are completely irresponsible and shamefully un-American. Greg's admonition against the dark side and his invitation to Hornberger to step into the light is a pitch-perfect model of how this kind of effort should be made. I am pleased to share it with you all, both so that Greg can be duly appreciated for this excellent work, and so that everyone else can benefit from this great example of how to proceed with similar neighborly efforts of their own directed at Hornberger and other "income tax Keynesians. Remember, friends don't let friends harbor and spread dangerous nonsense.

*****

"It is

difficult to get a man to understand something when

his salary depends on him not understanding it." THE TRUTH ABOUT THE INCOME TAX revealed in 'Cracking the Code- The Fascinating Truth About Taxation In America' (CtC) is NOT a matter of opinion, interpretation, speculation or fancy. CtC presents a simple syllogistic progression based entirely on easily-verified, indisputable facts. The facts involved in CtC's framework can be called "legal facts" perhaps, since they pertain to legal proceedings, relations and claims of various kinds. But this does not mean that any of these facts are matters of some legal interpretation. Instead, these core facts are simple, concrete realities entirely unreachable by judicial construction, opinion or interpretation. Because the core realities upon which CtC is founded are the bedrock that they are, any and all efforts to deny the book's revelations end up being exercises in misrepresentation, distortion and dissembling, as well as graduate-level examples of how to take material out of context either in a deliberate effort to deceive or out of a simple failure to understand that context. CtC's revelations are not disputed in these exercises-- they are creatively evaded, often by world-class twisters holding office precisely because of their skills at deception and evasion. This is true whether the denial effort is that of a judge, an attorney or an anonymous troll on a website. All such efforts, though, however creative and however shamelessly mendacious, founder on the rock-hard core facts. HERE ARE SOME OF THOSE FACTS (and please follow the links provided to see the proofs): Fact: The United States Constitution prohibits capitations and other direct taxes, except when laid according to the rule of apportionment. Fact: The Sixteenth Amendment does not repeal or modify these constitutional provisions-- it does not mention either of them at all, nor makes any claim to cause any such repeal or modification. Further, the US Supreme Court has said repeatedly that the amendment has no such effect. Fact: "Capitations and other direct taxes" are taxes "raised on the capital or revenue of the people", with "capitations" in particular being taxes laid on: "all that comes in"; "every different species of revenue"; "the fortune or revenue of each contributor"; "the [common-meaning] wages of labour"; "what is supposed to be one's fortune [per] an assessment which varies from year to year"; or "[an assessed percentage] of [one's] supposed [commonly-defined] income". Fact: The "income tax" is not laid according to the rule of apportionment. Inescapable consequence of the indisputable facts above: What is [lawfully] taxed under the unapportioned "income tax" does not and cannot reach "the capital or revenue of the people"; "all that comes in"; "every different species of revenue"; "the fortune or revenue of each contributor"; "the [common-meaning] wages of labour"; "what is supposed to be one's fortune [per] an assessment which varies from year to year"; or "[an assessed percentage] of [one's] supposed [commonly-defined] income". Instead, the unapportioned "income tax" necessarily can involve only a subclass of revenue distinguished from "the capital or revenue of the people" and "every species of revenue" by a definite, specialized and limiting characteristic. Further, it cannot be on anything which makes the tax EFFECTIVELY reach undistinguished revenue. WHAT'S MORE, Fact: The "income tax" is a federal excise. Fact: The subject of the "income tax" excise cannot be-- de jure or de facto-- the unprivileged, common generation, receipt, possession or transmission of capital or revenue. Were it so laid, the tax would be a capitation and would require apportionment, and be unlawful if, and to the degree it had been, administered otherwise. Fact: Excise-subjects involve the exercise of privilege. Fact: Everything specifically described in the tax law as subject to the tax is distinguished from the broad class of all similar things by being involved with the exercise of a federal privilege. Inescapable consequence of the indisputable facts above: Federal excises are taxes on the gainful exercise of a privilege granted by the federal government (which has, by virtue of its contribution to the gains through the granting of the privilege, a legitimate claim to a piece of the action). NOTE: The cognitive failure suffered by most folks who have difficulty grasping the true nature of the tax is to mistakenly imagine that the term "income" appearing in tax law and in judicial consideration of the tax must have the "unspecialized, all revenue that comes in" meaning of the commonly-used word (and to therefore struggle to harmonize with this meaning all else found in the law, such as by imagining to see "also" in places where it doesn't actually appear). The reality is that in the context of the tax, "income" (and related terms and provisions) have-- and can have-- only the limited, nuanced meanings by which the tax is able to conform to the foregoing immutable facts. The following little syllogism illustrates this:

It is with those conformant meanings and requirements in mind that the rest of the law must be considered and construed. Unsurprisingly, once this cognitive glitch is overcome, every single thing about the tax becomes startlingly clear and rational; more, with "income" construed as the core facts require, everything about the tax harmonizes fully with our founding principles, as well. *** I'M TOLD THAT A FEDERAL TAX COURT JUDGE issued a "memorandum" just last week in which he spends 31 pages attacking me and railing against CtC! I'm just guessing, but I'll bet that's about 5 times as much writing as the average entire judicial output in the disposition of a case. We can all be heartened by this extraordinary effort. Like others of its kind, this sweaty exercise is indicative of just how profoundly dangerous to its "ignorance-tax" gravy-train the state recognizes CtC to be-- because of how right the state actually recognizes CtC to be (as is proven for the a X 10,000th time by this week's Real American Heroes honored further down this page). Eventually, even the sleeping media is going to wake up and start reading between these lines. Interestingly, CtC wasn't even in evidence in the case in which this remarkable judicial agitation displays itself. The verbose judge apparently just decided to use his ruling in the case as an occasion to make a name for himself within his little special-interest world, like a 17th Century priest including a screed against Copernicus in his Sunday sermon. I probably don't need to mention where this guy's salary comes from... "First, they ignore you, then they laugh at you, then they fight you, then you win." -Mahatma Gandhi

“All truth passes through three stages. First, it is ridiculed, second it is violently opposed, and third, it is accepted as self-evident.” -Arthur Schopenhauer

*****

A Challenge To The Common Sense And Intellectual Integrity Of Skeptics, Doubters And Ostriches Lew, Jacob, Tom, Thomas, Alex, Glenn, Karen, Justin-- I hope you're reading, because I'm talking to you and YOUR readers, among others... PEOPLE, LET'S THINK LIKE GROWN-UPS for a while. I imagine we can all agree that people acting in their own immediate self-interest is evidence of nothing but the influence of human nature. In the same vein, we all know that when they see their immediate interest lying in NOT doing something, people can, and often will, find a million pretexts for not doing it. This is true of people acting independently and those acting as parts of an institution-- indeed, it is even more true in the latter case, where the institutional preference is the one being served. I hope we can all agree, too, that on the other hand, when someone acts AGAINST his immediate self-interest-- and especially when he acts against the self-interest of his institutional master, it is powerful-- even the most powerful-- evidence of a compulsion. That is, acting against one's immediate self-interest is plain evidence of the existence and compelling dominance of a higher interest. Testimony or admissions against self-interest are so axiomatically significant, and so obviously sound evidence in contrast to actions serving self-interest, that the former are given special weight in trials-- being deemed self-authenticating, and even being codified as exceptions to the "exclusion of hearsay" evidentiary rules. As the Advisory Committee on the Federal Rules of Evidence observed in proposing the exception as Rule 804(b)(3): "[T]he assumption that persons do not make statements which are damaging to themselves unless satisfied for good reason that they are true" provides the requisite "circumstantial guarantee of reliability" to make the hearsay statements admissible. Notes of Advisory Committee on Proposed Rules, Rule 804(b)(3).(As quoted by the 7th Cir. Court of Appeals in US v. Harty, 930 F.2d 1257 (1991).) Here's how such an admission is described in that "exceptions" rule: FRE Rule 804(b)(3) Statement Against Interest. A statement that: (A) a reasonable person in the declarant’s position would have made only if the person believed it to be true because, when made, it was so contrary to the declarant’s proprietary or pecuniary interest or had so great a tendency to invalidate the declarant’s claim against someone else... Testimony or assertions serving self-interest, on the other hand, are just as axiomatically suspect. We all know these things. To summarize, then (making use of the cited language to help prepare for what follows): Something done contrary to an actor's (or his institutional) proprietary or pecuniary interest, or which tends to invalidate his (or its) claims against someone else, is inherently evidence of the truth. On the other hand, actions favoring self-interest are inherently evidence of nothing more than the willingness of some people to do whatever seems to serve their immediate self-interest-- even if contrary to the truth-- when they are able to get away with it. All of this is common-sense 101. NOW WITH ALL THE FOREGOING IN MIND, I would like you to look at the following explanatory cover letter (especially you skeptics, doubters, fence-sitters and ostriches):

...which introduced this amended tax return; which produced this refund with interest:

(I know, many of you saw this victory two weeks ago, but bear with me, here...) NOW LOOK AT THIS EXPLANATORY NOTE that accompanied four complete "withholding" refund requests by a businessman:

...and the results (after a brief government effort to discourage the man with a "frivolous" notice):

NOW LOOK AT THIS COVER LETTER used to introduce this filing to the IRS:

...which resulted, after "frivolous" notices and an even clearer and more forceful iteration of the facts by the filers in response, in these:

NOW LOOK AT THE NINE HUNDRED or so other examples posted on this site. All are the same as these three particularly unmistakable selections to a greater or lesser degree. Some of those 900, like these selections above, include "Just so you can't even TRY to suggest that you misunderstood or were taken by surprise..." cover letters in the filing. ALL show only tiny amounts of income or none, and are accompanied by rebuttals of substantial "income" allegations by payers, making them just as unmistakable. Most report amounts withheld by those payers, as well, and reclaim every penny-- Social Security and Medicare taxes along with the kind simply called "federal income taxes", making them unmistakable. Many are the second, third, fourth, fifth, sixth, seventh claims and complete refunds to the same persons or couples, which have been being submitted and honored year after year. OKAY, A LITTLE BIT OF YELLING NOW (remember, this is just at the skeptics, doubters and ostriches, who have been keeping the truth at bay for all of these ten years now): PEOPLE! THINK IT THROUGH! NOT ONE OF THESE EXAMPLES-- OR THE TENS OF THOUSANDS OF OTHER IDENTICAL EVENTS OF WHICH THEY ARE A MERE REPRESENTATIVE-- NOT ONE, WOULD HAVE HAPPENED EVER IF CtC WEREN'T ACCURATE AND CORRECT IN WHAT IT HAS BEEN TRYING TO TEACH YOU ABOUT THE TAX AND THE LAW!! C'mon, people, I called for your "grown-up" at the beginning-- put on that hat! Face the disquieting truth...Heck, EMBRACE the liberating, empowering, state-restraining truth!! These tens of thousands of admissions have been made and continue to be made even though the agency's immediate institutional self-interest (and outright 'mission statement') is to:

Plainly, in every one of these cases, the agency bowed to the overarching, compelling interest of compliance with the actual law concerning the tax. The evidence is before you and unmistakable: When the government does things "by the book", it acknowledges, honors, and admits what CtC has revealed about the tax and the law. (This is not to mention the fact that every single filing claiming a refund-- and especially those as readily-distinguishable and out-of-the-ordinary as CtC-educated filings-- are challenged by default. See here and here. The simple, glaringly-evidentiary fact is that every check and credit issued in response to a CtC-educated claim has passed through the gauntlet and been approved.) I know this may come as a shock to you (since you've been managing over the years to not look at any of what I am showing you now, and so have managed to avoid the chain of logic we've just followed). But there is nothing to be surprised about here. This material shows EXACTLY how the tax came to be misunderstood and eventually misapplied on a massive scale, with that misunderstanding and misapplication becoming the Kool-Aid on this subject you've been forgivably imbibing your entire life. Forgivable until now, that is. Now you can't even pretend to not know, or not understand. Now you can't fail to recognize that every pretense of tax agency resistance to CtC and to those who make use of its revelations, and every effort to discourage those folks IS NOTHING BUT A PRETENSE-- and a corruption, and a defiance of the law. Now you can't fail to recognize that what really SHOULD have gotten your skepticism antennae humming were the unprecedented assaults on CtC. In the new illumination with which you are now equipped, consider the never-before-in-American-legal-history injunctions attempting to dictate the sworn testimony of American citizens, and to exercise prior restraint over future testimony the government finds inconvenient. Both of these egregious, manifestly-unconstitutional assaults are still being pursued in federal courts to this day, and now that you understand the truth, do you not now also understand that these actions (and the much-ballyhooed prior "rulings by the courts against CtC" of which they are a part) are pure corruption in service to a status-quo of general misunderstanding of the tax? Just as are the equally-transparent discouragement contrivances by which some educated filers are harassed; and that properly understood, both are themselves evidence of the truth against which they are obvious dodges and evasions? Do you not understand that the state has been forced to resort to these manifestly-unconstitutional and epiphany-risking measures because it knows the misunderstanding of the tax they are meant to preserve is existentially significant to its illicit ambitions, even if you had not understood that significance before? Don't you now recognize that significance, and the importance of you (and everyone) dispelling the misunderstanding and denouncing the corruption? Don't you now recognize the critical importance of you and everyone else acting in harmony with the truth about the tax? If You Have, Aren't You Really, Really Glad YOU'VE Taken Control Of How Much Of YOUR Money Washington Gets To Spend, Just As The Founders Intended?

If You Haven't, ARE YOU CRAZY??!!

Seriously! WHAT THE HELL IS WRONG WITH YOU??

LEARN the liberating, empowering, critically-important truth about the 16th Amendment and the liberating, empowering, critically-important truth about the "income" tax. STOP merely reading (or writing) about how bad things are and START DOING SOMETHING ABOUT IT!

“Most of the important things in the world have been accomplished by people who have kept on trying when there seemed to be no hope at all.” ‑Dale Carnegie

***** My Friends, This Time I Ask: What Are YOU Doing Wrong? I've got "the will", but by myself, I don't have "the way"... YOU PROBABLY ALL KNOW THAT THE IRS, DOJ AND A FEW "IGNORANCE TAX"-INVESTED INDEPENDENTS maintain webpages as part of the ten-years-and-counting campaign to sow disinformation and fear about CtC. These pages are erected for the purpose of preventing Americans from reading CtC and learning the truth about the tax in the United States version of book-burning (in which the proscribed material is left out there, but highly-sophisticated, ultra-high-density propaganda is devoted to discouraging people from wanting to read it in the first place). Every now and then, I hear from a visitor to one of these troll-pages. Most of these folks write to share their wry amusement at the transparent evasions, misrepresentations and omissions by which these discouragement efforts are distinguished. These evasions, misrepresentations and omissions are recognized by the discerning visitor as the most sincere affirmation possible of CtC's revelations. They are admissions against the interest of those making the posts, who feel obliged to address the book, but must resort to strawmen and obfuscation due to being unable to attack what it actually says. A GREAT EXAMPLE IS THE ASSERTION BY DOJ ATTORNEYS-- over signatures, no less, and in a formal filing in a 2006 court case against me personally (and my wife, Doreen), that CtC argues that, "only federal, state or local government workers are liable for the payment of federal income tax or subject to the withholding of federal income, social security and Medicare taxes from their wages under the internal revenue laws." This is ridiculous, of course, but the government attorneys had to make an assertion that the judge in the case could cooperatively declare to be false, in order to have a pretext for an adverse ruling. Similarly, these attorneys claimed in their appellate court filings that CtC makes the absurd argument that "wages" are not "income". In both cases-- in the district court and in the appellate court-- the compliant judges simply took the DOJ at its word (vehement, expert and thoroughly-documented rebuttals of these easily-exposed falsehoods notwithstanding). But that's really the least of it. The whole affair was an exercise in avoiding any real contest. The "ruling" in the district court was actually just the granting of a government motion for "summary judgment" (with our demand for a trial being simply ignored without explanation, despite fact-issues being thoroughly in dispute). The judge simply signed an entirely-prosecution-written "ruling". (We were copied on it when the DOJ attorneys filed it for the judge's signature.) This "ruling" included, and simultaneously based itself upon, a batch of purportedly "found facts", among which are mere assertions by a government declarant which were admittedly informal and non-testimonial (and therefore utterly meaningless). Unsupported, government-serving third-party assertions were accorded the same treatment in the DOJ-written "ruling". All are "found as facts", and form the basis for the "ruling", despite being formally disputed and despite there never being so much as a single hearing in the case. These same fraudulently "found facts" were adopted without question by the appellate court in turn, making its own rulings equally invalid foregone conclusions, and the like product of an exercise in evasion rather than the outcome of an actual impartially-refereed adversarial test of truth, facts and law. But these are the "victories" in the civil case the DOJ has touted ever since as "rulings by the courts against CtC". (I mention only a few of many revealing ploys and evasions involved in this case-- read more about it here.) Two-and-a-half-years later, with CtC's revelations continuing to spread, and with more and more Americans rising to act on behalf of the rule of law (and despite repeatedly failing to get a grand jury to issue a real indictment), the government announced unsigned charges alleging that I don't believe what I have written two books and countless articles and essays about, and what the federal and state governments have been steadily acknowledging to be true for more than ten years now in tens of thousands of cases. I was tried on these charges a year later in a shameful kangaroo affair. In that sham of a trial, all the government's civil case material described above was presented as "evidence" against me to the jury, while I was denied an opportunity to question any witness about any of it. I was not allowed to put any expert witness on the stand-- not even an IRS agent. The jury was denied sight of the actual statutory definitions relevant to the case, and instead instructed to deliberate using prosecution-written "interpretations" of those definitions. There is much more-- see a comprehensive, documented discussion of this railroading here. Like the contrived and fraudulent outcome of the "civil case" before it, the foreordained conviction in this criminal assault is touted by IRS, DOJ and invested "independents" as "rulings against CtC". What these rulings REALLY amount to, of course, are admissions by the DOJ that what CtC REALLY says can't be refuted. If anything the book REALLY says could be refuted, it surely would have been presented for that treatment in these contests-- the purpose of which was to discourage people from reading this material. Each of these lies against and about CtC is thus an admission that its truth is unchallengeable. As was observed by Heinrich Himmler, the Nazi's master of the art, "The lie is the truth, only backward. Hold up the lie to a mirror, and the truth will be staring you back in the glass." UNFORTUNATELY, MOST FOLKS NOT ALREADY CtC-EDUCATED ARE taken in by these propaganda posts, and especially by the representations on these troll-sites of these purported rulings against CtC by federal courts. These misrepresentations have their particular effect for two reasons. One reason is that a certain amount of effort is needed to winnow out just how a court ruling evades the actual issues presented. It is almost always necessary to read one or more legal briefs or memoranda just to see what the court is side-stepping or conveniently "misunderstanding" (plus, of course, it would be necessary to actually read CtC...). The other, and more significant reason (because in some folks it halts all investigation before it begins), is that many Americans continue to be under the thrall of a childhood-implanted delusion that judges are impartial, diligent upholders of the truth, rather than the deeply partisan political hacks that far too many of them really are. Those taken in by childish respect for the courts are pre-empted from doing their own discovery of the facts, and applying their own reasoning to the issues. They prompt an image of a civil rights activist in the early '60s shrugging his shoulders and hanging it up, muttering, "Darn! Segregation sure didn't seem right to me...!" upon merely learning that federal courts had upheld it (and even at that the analogy is weak, because here the courts have NOT actually held against the truth about the tax, but only against a very deliberately-contrived strawman). Or perhaps this is a better analogy today: People being dissuaded from learning the liberating, state-restraining, republic-restoring truth about the tax by finding a note from the DOJ on its door saying "Don't bother, the courts have ruled against this..." is like everybody saying, "Well, strange though it may seem, apparently mass warrantless spying on all Americans by the government DOESN'T violate the Fourth Amendment, 'cause that's what federal courts have said...!" Pretty ridiculous, no? SO, here's my question for you all. WHY AM I THE ONLY ONE WRITING ARTICLES LIKE THIS??!! Do you think that if Martin Luther King hadn't been just one of many voices exposing and denouncing the pretenses and railroadings-- moral, intellectual and legal-- by which the unconstitutional injustice he addressed was sustained and defended, his cause would have ended up on the front page and the evening news, and thus eventually given its due in the government's courts? Do you think that if Edward Snowden were the only one writing about the illegitimacy, Constitutional irrelevance and outright pretenses and evasions of FISA court pronouncements and approvals that the country would be as close to up in arms over rampant government Fourth Amendment crimes as it is today? HERE IT IS, PEOPLE: It will only be YOUR postings and YOUR sending of the sort of thing I've just discussed above that will have a chance of inoculating YOUR neighbors, YOUR bosses, YOUR lawyers and YOUR family against the government's cognitive viruses. IT WILL BE WHEN EACH OF YOU, IN YOUR THOUSANDS, have written, posted and shared your own testimony regarding the "rulings by the courts" and regarding what YOU know to be true about the tax-- on your own sites, in newsgroups and chatrooms, as blog comments, and in letters-to-the-editor-- that the shameful silence of even the most "alt" of even the "alt-media" will end. Only then will YOUR CAUSE-- the moral, intellectual, and legal correctness of just saying NO! when Audrey II bellows, "FEED ME, SEYMOUR!"-- hit the headlines. Only then will the liberating truth about the tax begin to prevail.

Here's Audrey II, grown up from the cute little relatively harmless thing she once was into just shy of what she's about to become-- a powerful monster that takes what she wants-- all because Seymour kept feeding her when he should have known better...

"A nation of sheep will beget a government of wolves." -Edward R. Murrow

"Be the change you want to see in the world." -Mohandas Gandhi

|

||||||||

{kind=link}

{kind=link}