|

More Victories For The Rule Of Law- Page Forty-Seven

Tens of thousands of readers of 'Cracking the Code- The Fascinating Truth About Taxation In America' have taken control of their own resources, in accordance with, and respect for, the law. The likely total amount reclaimed by these good Americans so far is upward of several billion dollars.

A few of these good American men and women-- such as those honored below-- are generous enough to send me the evidence of their victories in upholding the law, for the edification and inspiration of everyone. At the moment those shared refund checks, closing notices, and so forth total:

Dennis O'Connell

There is some IRS evasion associated with this victory-- see the story as episode 45 of the 'Every Which Way But Loose' collection!

From this:

to this:

Mike had filed "ignorance tax" returns for 2011 prior to finding CtC and learning the liberating truth about the tax. He then amended both his federal and California filings in light of his new knowledge.

In the meantime though, both the feds and California had demanded payment of what had originally appeared to have been taxes due-- the feds for some $50,000+ along with penalties and interest, and California for more than $15,000 plus penalties and interest.

Mike's educated amendments changed night to day. In October 2012, soon after receiving Mike's amended federal return (and after engaging in a modest bit of fuss), the feds reversed their assertions and Mike's "balance due" became a refund check. See that victory for the rule of law here.

In January 2013, Mike sent in his amended California return, and after a few stutters while the new information was processed, California's demands for payment also turned into a full refund of everything Mike had paid to the state. The full documentation can be seen here.

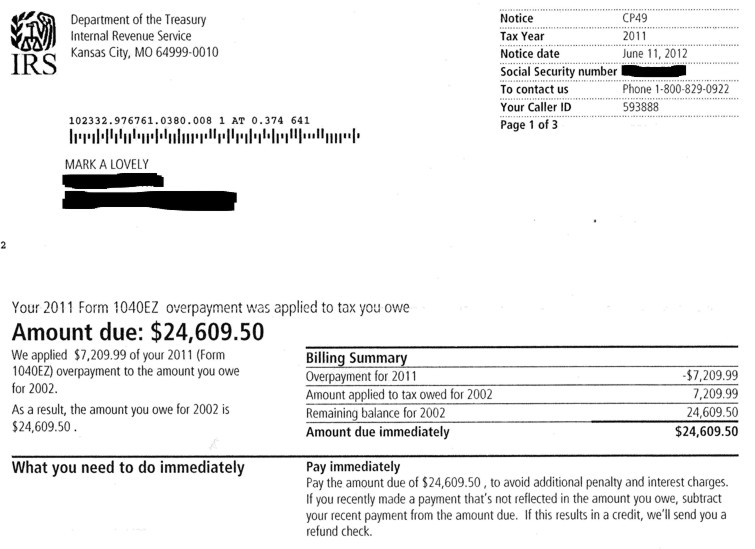

Mark Lovely

Don't be misled-- while this refund notice makes what the IRS alleges to be owed for a different year the most prominent feature, this is, in fact a notification that Mark has been refunded everything withheld from him during 2011-- Social Security and Medicare taxes included (see the "Billing Summary" section). The amount has simply been gratuitously diverted to pay off what the government purports to be a debt owed to it by Mark.

Enjoy Mark's previously posted federal victories for 2008 and 2009 here and here.

Joseph Davis

Don't be misled-- while this refund notice makes what the IRS alleges to be owed for a different year the most prominent feature, this is, in fact a notification that Joseph has been refunded everything withheld from him during 2011-- Social Security and Medicare taxes included (see the "Billing Summary" section). The amount has simply been gratuitously diverted to pay off what the government purports to be a debt owed to it by Joseph.

See the filing that led to this victory here.

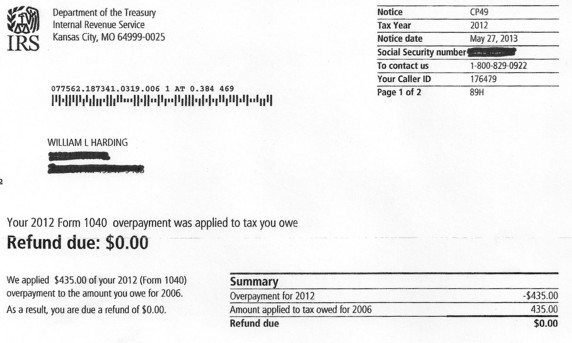

Bill Harding

(2012)

See the filing that led to this victory here. Enjoy Bill's federal victory for 2008, and his Michigan victories for 2005, 2006, 2008, 2009 and 2011 (and his federal victory for 2012 below on this page).

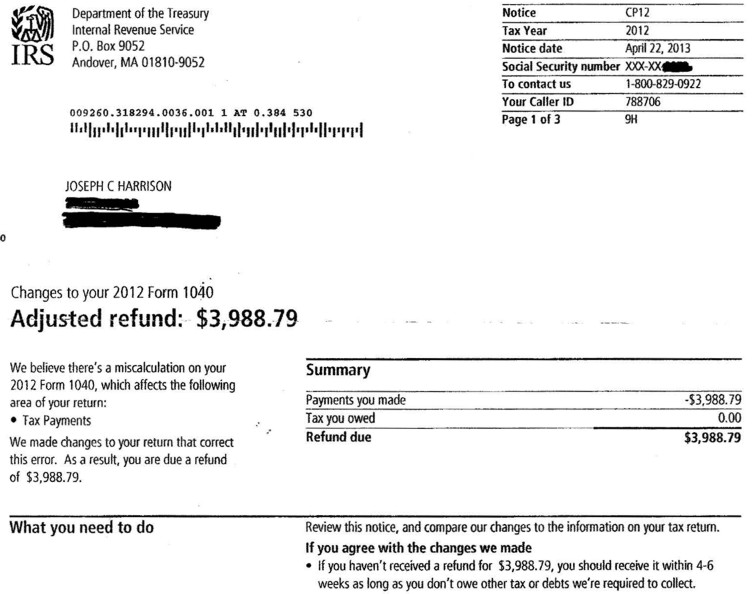

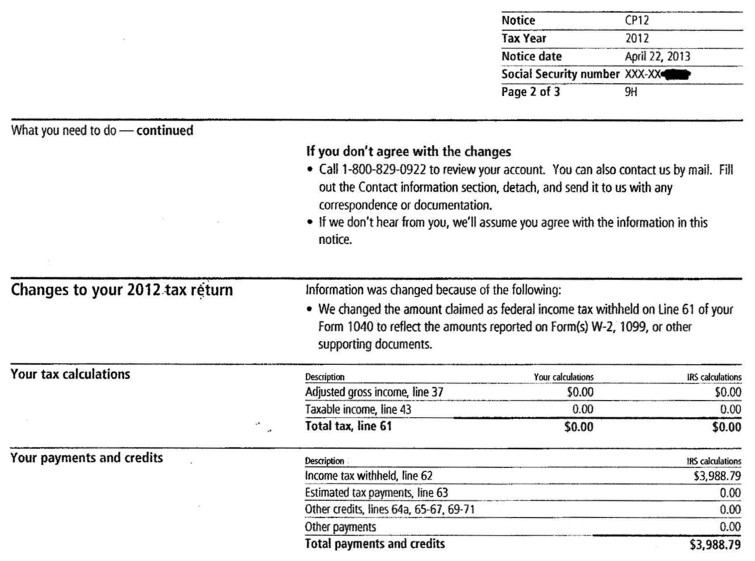

Joseph Harrison

Joseph had neglected to rebut a 1099-C alleging a taxable gain to him as a result of forgiveness of a debt by a federal institution in the course of its "trade or business". The IRS told him a tax was therefore due and owing (along with other adverse consequences):

Joseph responded with these, declaring that the debt that was forgiven had nothing to do with any "trade or business". The IRS agreed, without a fuss:

During the same period that the docs in this little 2011 kerfuffle were going back and forth, Joseph was invoking the law and reclaiming what had been errantly withheld from his earnings as "federal income, Social Security and Medicare taxes" under the presumption that those earnings were a consequence of Joseph's conduct of taxable activities. Joseph corrected the mis-impression with forms specified by the US Treasury for this purpose-- forms 1040 and 4852 (see Joseph's here)-- and promptly received IRS agreement with his conclusions:

A Treasury check also arrived:

Annoyingly, although Joseph is doubtless pleased to have gotten some of his property returned so far, this check is only for all of what was withheld as nominal "federal income tax". Not yet returned is what was withheld from him as Social Security and Medicare taxes. See Joseph's filing to see what is missing.

Social Security and Medicare taxes ("income" taxes like any others, despite having their own special names and being technically "surtaxes") only arise under the law in concert with the receipt of "wages". Both Joseph and the IRS agree that none of those were received, so the government's failure to return the amounts withheld as such is inexplicable and indefensible, (and as a practical matter, means that Joseph will be put to some very undeserved trouble seeing to it that he is made whole).

K. & S. G.

See the docs that produced K. and S.'s debut victory here. It will be noticed that this refund is about $800 shy of the total withheld and the couple's corresponding claim. They say they made a mistake handling the 1099-R, and also had a few hundred nicked off this refund for an alleged liability from a previous year. K. says he'll be doing some amending...

T.

This victory for 2012 is T.'s first on behalf of the rule of law!

Bill Harding

See the filing that led to this victory here (Bill deliberately declined to recapture what had been withheld from him as the FICA income taxes, as he is currently accepting the benefits from that program and feels this is the right way to deal with that situation). Enjoy Bill's federal victory for 2008, and his Michigan victories for 2005, 2006, 2008, 2009 and 2011 (and for 2012 above on this page).

Noel Berube

See the filing that produced this debut victory here.

L. W.

See the filing that produced this debut victory here.

Click here to return to the Bulletin Board

Even in the face of the requirements of the law, the junkyard dog still tries to play its losing hand occasionally. Ironically, it is these sporadic spasms of resistance that offer the most telling evidence of the truth about the tax...

Despite the fact that those whose victories are on display here did nothing but insist that the law be applied as it is written, they did so in the face of fearful threats and cunning disinformation from the beneficiaries of corruption. Their actions took great courage and commitment, and I salute them all. “God grants liberty only to those who love it, and are always ready to guard and defend it.” -Daniel Webster

NOTE: Whether any given individual is entitled to a refund depends on a number of different factors, and no one should presume that they are so entitled simply because they see that others are. Each person should educate himself or herself about the particulars of the law, and make his or her own determination in this regard. |

To get on the Lost Horizons mailing list, send an email to SubscribeMe 'at' losthorizons.com with your name in the message field.

The First Complete "Income" Tax-Related Refund (Social Security, Medicare And All) Ever Received

An "Income" Tax Subject Site Map

A Few Words About Tax "Reform"

NOTE: The documents displayed on this and any linked pages, and any associated comments, are posted with the permission and cooperation of the upstanding Americans with whom they are concerned.

When a return is posted in connection with any refund or other responsive document, it is complete-- that is, what is posted is EVERYTHING filed as a return in connection with that refund or document, unless otherwise indicated.