|

Frequently Asked Questions Page Two

READ EVERYTHING THAT

FOLLOWS CAREFULLY AND THOROUGHLY

Although material on this page is

organized topically, don't assume that you can identify what you

should read by picking among the topics. Some material

which is very important to a complete understanding of one

subject area may be found in several different places.

READ THE WHOLE PAGE!

Every individual is responsible for his or her own overall

education, conclusions and decisions, regardless of what may be

read here. Also, those who find their way here but have

not yet read 'Cracking

the Code-The Fascinating Truth About Taxation In America'

might find much of what follows cryptic and/or confusing.

Read the book.

No

other source of information on this subject will suffice-- in

fact, most will simply make the truth difficult to understand.

Indeed, even those who HAVE read the book should be wary in

regard to other sources of information. Many tax

"theorists" and soapbox orators have studied

CtC

themselves and have incorporated elements (or even a great deal)

of what they have learned into their own presentations.

Thus, such presentations may appear on the surface to be soundly

based. However, since these partial-adopters have also

clung to elements (or even a great deal) of their original

misunderstanding, they continue to promote much error-- which is

now just better concealed, or more convincingly presented, than

before.

Click here for more on this.

If needed, click

here for a brief review of the truth about the income tax.

A Lost Horizons "Income" Tax-related Site Map

|

The following links will

take you to the indicated FAQ topic area (but everyone is strongly

encouraged to read this whole page-- material located in one

topic area can often significantly help in understanding the nuances of

a different topic area):

Recent Changes

In The Appearance Of Form 4852

About "Natural" Versus "Artificial" Persons

About "Excess Social

Security and Tier 1 RRTA Tax Withheld"

There

IS "A Law", And This Is How It Works

A Thumbnail

Sketch Of The "Income" Tax Reporting And Determination Process

Does It

Matter If I...

Regarding

Capital Gains, Etc.

Does Filing Initiate

An "Administrative Proceeding"?

What About Getting

Loans?

Is It

Necessary To Make Legal Arguments In A Filing?

Does Submitting A W-4

Make One Into An "Employee" (Or Constitute An Election To Be Treated

As One)?

A "Wage" By Any Other Name Is Still Taxed The Same...

Does Using Federal

Reserve Notes Make An Activity Taxable?

What About Being

Licensed?

Are Activities As

A Public School Teacher Subject To The Tax?

What About Bitcoin?

Frequently

Asked Questions Page One

|

Q. The new Form 4852 is

different from the one in the appendix of CtC. Is

this significant?

Yes, and here's why:

EVEN WHILE MAKING

TENS OF THOUSANDS OF GOVERNMENT ADMISSIONS TO THE CONTRARY

in response to CtC-educated filings over more than ten years

now, and even through repeated form revisions over that

period, the US Treasury Department persisted in accompanying

its "Form 4852 [substitute for incorrect or missing Forms

W-2 or 1099-R]" with language suggesting that the form could

only be used by "taxpayers", and that to use the form, or to

report withheld amounts, was to declare (or agree) that

"taxable income" had been paid. At long last, this

misleading language has been withdrawn and replaced, in a

tacit admission of the truth about both matters.

The faulty and misleading language had never

appeared in the actual declaratory content of the form, of

course. Instead, both false ideas were conveyed by inviting

assumptions from phrasing in the "instructions" published

with the form.

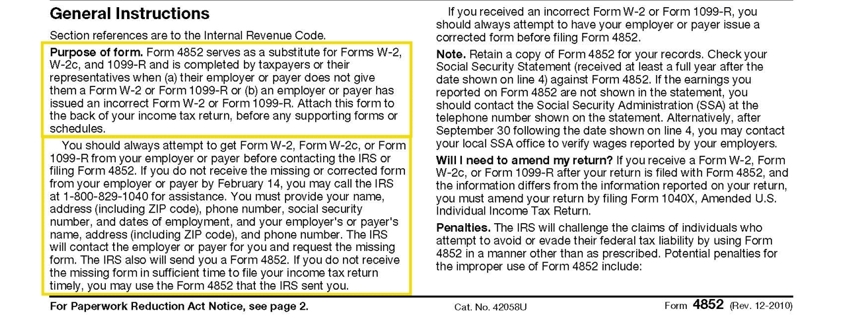

For instance, the "Purpose of Form" instruction

accompanying prior versions declared that, "Form 4852 is

completed by taxpayers or their representatives..." The

casual reader was thereby invited to assume an "only" in

that declaration, even though none actually appears.

Also carefully kept out of the form's

declaratory content, and thus never crossing the line into

directly implying that adverse inferences attend the use of

the form as a legal matter while still being predictably

misleading, language in the "Line-by-line" portion of the

previous versions' instructions read, "Line 4.

Enter the year the taxpayer had taxable income from which

Federal taxes were withheld..."

In addition to appearing merely in the

instructions and plainly reflecting self-serving assumptions

about who would be using 4852s (in harmony with the

revenue-hungry state's default position that any given

economic activity is of the taxable variety unless and until

declared otherwise by the actor), neither of these

misleading expressions were definitive or pre-emptive. As

noted above, there was no "only" in this language.

But at the same time, the retention of this

misleading wording even after a growing number of Americans

began using 4852s to rebut allegations of the receipt of

"income", and despite several revisions of the form--

including revisions of the instructions-- each plainly in

direct response to this new application of the form, was

unquestionably a deliberate effort to corruptly encourage

uncertainties and anxieties about this use of the form.

Happily, some honest individual or group at the Treasury

Department couldn't stomach the deception any longer, and a

few months ago, the 4852 was revised yet again, this time

with the misleading language removed.

(It's possible that honesty had nothing to do

with this new, improved revision... Perhaps the change

occurred due to virtuous push-back by CtC warriors.

No one has ever faced an assertion that 4852s

couldn't properly be used as the CtC-educated use them. But

some have had occasion to debunk a ridiculous assertion that

amounts can only be withheld from "income" payments, and

that therefore declaring that amounts have been withheld is

to declare that "income" has been paid, made by an IRS or

DOJ hack floundering about for an adverse argument in a

legal contest. See some discussion of this subject

here.

This latter "argument" is so patently

untenable and embarrassing even just to read or hear-- and

so readily debunked by simply inserting a big red

"properly" into it, as, "amounts can only

properly

be withheld from "income" payments..."-- that someone in a

position of authority may well have commanded that it be abandoned.

After all, to trot out such a desperate argument, or even just to allow it to be

suggested by the 4852 instruction language, is to more

overtly admit to having no argument against a CtC-educated

claimant than to simply say nothing...)

SO, LET'S LOOK AT HOW THE 4852 WAS BEFORE CtC

and how it was changed in several revisions intended to

discourage the educated CtC community (even while its

members' claims continued to be routinely honored). Then

we'll look at what it has now become in a tacit admission of

the CtC-revealed truths the state still finds hugely

inconvenient to its unbridled ambitions but no longer dares

to deny in this fashion.

At the time of CtC's publication in 2003

the 1998 version of the form was the current version.

Page 1 of that form-- the only page at which anyone HAD to

look, since it's the one with all the "action" elements--

presented nothing at all capable of affecting one's view of

the form's utility. Here is the bottom portion of that page,

where we find the only text on the page which is not part of

one of the fields to be completed:

On page 2 of the form we find the old portions

of text which are the subject of our discussion, and which

were, pre-CtC, not unreasonable in their inclusion. After

all, pre-CtC, it is likely that the form would never have

been used other than by someone who believed both

expressions to be apt and unremarkable:

At the end of 2005,

after the IRS had begun to be inundated with CtC-educated

filings as word of the liberating truth about the tax

spread, Form 4852

was revised. The "Paperwork Reduction Act" notice was

shouldered off page 1 by the misleading "Purpose of Form"

language (and some additional

somewhat-discouraging-appearing material brand new for this

revision). This change was plainly intended to deceive and

discourage the growing army of newly awakened and upright

ex-coppertops:

At the same, time, a slight change was made in

the "Line 4" instruction which remained on page 2 ("the

taxpayer" is replaced by "you"):

By early 2007,

CtC-educated claimants were recovering all their money

in ever-greater numbers. This was both for the simple reason

that the liberating truth about the tax continued to rapidly

spread, and because in April of 2006, the government had

launched

a new, transparently corrupt effort to discourage that

spread which predictably backfired due to its

particulars constituting unmistakable evidence of both the

accuracy of

CtC's information and the importance of that information

being acted upon by every grown-up American with a smidgen

of common-sense and love of country.

Still in its reflexive stonewall mode, the

government rolled out another revision of Form 4852,

retaining the misleading "Purpose of form" language on page

1 and adding penalty warnings which had never appeared

anywhere on the form or its instructions in the past:

Page 2 of the form was essentially unchanged

other than as necessary to account for the fact that some

line numbers on the form had been changed. The misleading

"line 4" language remained the same.

The return of improperly-withheld and -paid-in

amounts by the federal and, by then, 33 state tax agencies

and treasury departments ratcheted up during the subsequent

several years. Within a year of this 2007 revision just the

tiny fraction of these refunds

generously furnished to me for posting and sharing with the

world had reached a pace averaging $83,000.00 per month.

However, rather than just face the facts like a man and

reconcile itself to

the unchallengeable legal reality it was quietly acknowledging with every refund check, the

government doubled-down, as is its reflex. In late 2008, after

years of internal proposals to try to charge me with

something in order to frighten people away from CtC--

each of which was declined by the IRS's own "criminal

division"-- and despite its failure to secure a real

grand jury indictment, the DOJ "tax division" in

Washington produced an unsigned "indictment" charging me

with not really believing that my earnings don't qualify as

"wages" (under a special tax-law "perjury" provision).

A suitably manipulated show-trial followed a year later,

resulting in a foreordained conviction.

As with the similarly-bogus, similarly

truth-emphasizing "civil lawsuit" attack, this criminal

assault just galvanized truth-fueled, truth-spreading

American men and women. Even after I checked in at a federal

prison, refunds based on what I was charged with not

believing to be true continued to be demanded, and continued

to issue forth, week after week.

Again desperate to frighten the people away

from the inescapable, but oh, so inconvenient truth, the

feds cranked out yet

another revision of Form 4852 in late

2010. (It's worth noting at this point that prior to 1998,

Form 4852 had not had a single revision of any of the

varieties discussed here in all its prior 24 year history. A

number of forms had been issued during those years--see

here,

here,

here,

here,

here and

here-- but the changes in all these cases simply

involved some tweaking of the formatting, responses to the

OMB-numbering requirements introduced in the 1980s, and the

addition of pension-return applications.)

The 2010 revision again retained on page 1 the

misleading, misstated "Purpose of form" language and kept

the beginning of the threatening "penalty" section

front-and-center. New was a chunk of actual gibberish,

apparently added by a bureaucracy in such a lather to order

the tide to recede that either no time was spent

proof-reading the work or the level of desperation had

reached the point at which resort was being made to sheer

confusion. Look at the second highlighted paragraph (below

the "Purpose of form" language, which remained as it had

been in prior versions):

Enjoy this. ON THE FORM 4852 IN YOUR HAND you

are advised to contact the IRS so that... it can send you a

Form 4852...? Somehow, I suspect that if a CtC-educated

person were to climb through this looking-glass and get an

IRS agent on the phone what he or she would receive would be

nothing helpful. But I'm a cynic by nature (well, by

experience, really).

Anyway, this gibberish was the sole addition

and apparent reason for the 2010 revision. The material on

page 2, the "Line 4: Enter the year you received taxable

income from which federal income taxes were withheld"

included, remained virtually identical to the corresponding

instructions on the page 2 accompanying the 2007 form:

SO, QUITE A LITTLE CAMPAIGN TO DISCOURAGE,

INTIMIDATE AND CONFUSE educated Americans from successfully

making their inconvenient rebuttals and reclamations over

the first ten years since

CtC first revealed the liberating truth in 2003!

FINALLY, though, someone has found

him-or-herself obliged to excise the overt,

egregiously-misleading "Purpose of form" and "Line 4"

language previously clung-to on these forms over all those

years and through all those revisions.

Finally, the effort to falsely imply that

the Form 4852 is only for use by "taxpayers" (and to falsely

imply that use of the form supports a presumption of

self-endorsed "taxpayer" status) has been abandoned.

Finally, the effort to falsely imply that

"withholding" can, as if by a law of nature, only

be applied to "taxable income" (and to falsely imply that

reporting amounts withheld implies an agreement that what

they were withheld from was "taxable income", whether the

"wages" variety or any other) has been abandoned.

That long-standing misleading language has

FINALLY been replaced with new expressions acknowledging

that NON-"taxpayers" also can and do use these forms, and

that reporting amounts withheld says nothing whatever about

the propriety of that withholding, or the legal character of

what it was withheld from.

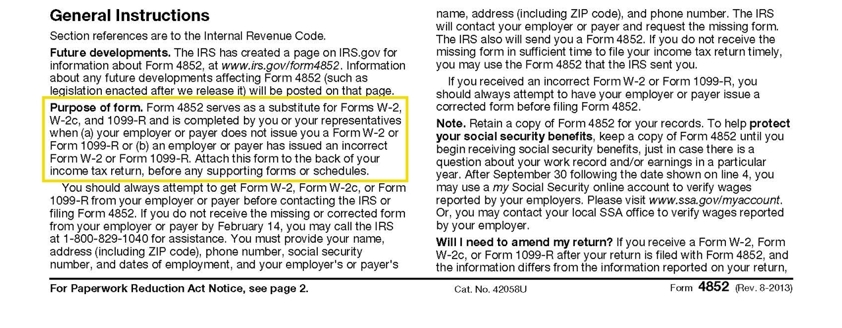

In August of 2013-- exactly ten years after the

publication of

CtC, the Department of the Treasury

replaced previous versions of Form 4852 with its

new, much-improved model, acknowledging every

CtC--thing about these forms. Here is page 1, with the

new, straightforward "Purpose of form" language:

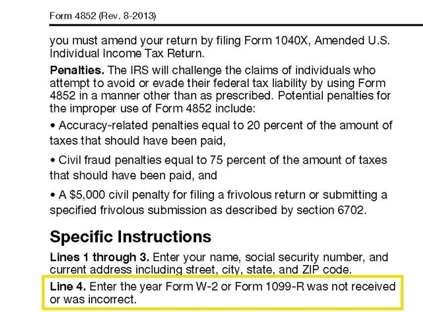

Here is page 2 of the new form, with the new,

no-longer-flogging-the idiotic-withholding-argument "Line 4"

language:

It's about time. P.S. In 2014, the

signature line was removed from the form. Not a

significant change, in my view, as a form attached to a

1040 is covered by the 1040 attestation anyway.

BUT WAIT, THE EFFORTS TO DISCOURAGE,

INTIMIDATE AND CONFUSE educated Americans have

resumed in 2020! Now we see another change in the form,

and one plainly meant to be misunderstood.

The new form begins with a statement appearing to

require a user of a Form 4852 to confront a payer and

demand a W2c or corrected 1099:

Anyone not tuned-up in agency tactics would almost

certainly be misled into thinking that unless they make

that confrontation, possibly endangering their

relationship with the payer, they must abandon plans to

use the form to rebut an incorrect W-2 or 1099-R. Such a

misled person might very well be discouraged and

dissuaded from reclaiming their property.

The educated filer, of course, will recognize the need

to look further. Doing so will be fruitful.

AT THE BOTTOM of page 1 of the form the general

instructions will be found, and here we find the

reference to an "Attempt to get..." put quite a bit

differently:

Suddenly, "must" becomes "should", and the incongruous

proposition that you can only rebut an errant payer's

assertions if you have tried to convince him to change

his statements is revealed as a deception (or, at least,

is flatly contradicted). Continuing on to

page 2 of the form, we see the "deception" conclusion

ratified yet again. Here, the instruction for "Line 10"

on the form asks for an explanation of "any attempts" to

get the payer to change his tune, rather than "YOUR

attempts", as it would say if you really were required

to make such attempts:

How tiresome these people can be! |

|

Q. You say in your

foreword (7th edition and earlier):

"Corporate

managers, though, are warned that this book does not

directly address the peculiarities of the "income" tax

as it applies to artificial persons." Does

this mean that "income" means something different for

artificial persons than what it means for "natural

persons"?

A. Not at all. "Artificial persons" are

relevantly viewed by the law in precisely the same

fashion as "natural persons", and both are taxed on the

same activities, and nothing but the same activities.

"Income" means the same thing for both; and the gains of

artificial persons are not "income" simply because the

one enjoying the gain is an artificial person, even in

the case of a federally-created artificial person

(although it is almost certainly the case that

pretty-much every gain enjoyed by most federally-created

or controlled artificial persons will be from the

conduct of a taxable activity).

The "disclaimer" language you cite simply reflects the

fact that I devote very little of CtC to discussing how

state-chartered corporations (or LLCs, etc.) are made to

appear to be federal or federally-controlled

corporations ("domestic corporations", or "corporations

organized under the laws of the United States", etc.).

(See

this for

additional material on this topic.)

|

|

Q. Is the "Excess Social

Security and Tier 1 RRTA Tax Withheld" line on a

1040 the proper place for reporting or reclaiming

what is withheld from non-"wage" earnings under the

names "Social Security and/or Medicare taxes" (and

should "Form 843" be used for this purpose)?

A. No. The following explanation of what

that line IS for (and what "Form 843" is for, as

well) is taken from the IRS online "Tax Topics"

collection, topic #608:

Most employers must

withhold social security tax from your wages.

Certain government employers (some federal,

state, and local governments) do not have to

withhold social security tax.

If you work for a railroad

employer, your employer must withhold Tier 1

railroad retirement (RRTA) tax and Tier 2 RRTA

tax.

If you had more than one

employer and your total wages were over the wage

base limit for the year, too much social

security tax or Tier 1 RRTA may have been

withheld. The wage base limit for the year can

be found in the Form 1040 Instructions. If you

had more than one railroad employer, and your

total compensation was over the maximum amount

of wages subject to Tier 2 RRTA, too much Tier 2

railroad retirement (RRTA) tax may have been

withheld. If you had too much social security

tax or Tier 1 RRTA withheld, you may be able to

claim the excess as a credit against your income

tax. If any one employer withheld too much

social security or RRTA tax, you cannot claim

the excess as a credit against your income tax.

Your employer should make an adjustment of the

excess for you. If the employer does not make an

adjustment, you can use Form 843 (PDF), Claim

for Refund and Request for Abatement to claim a

refund.

If you are claiming excess

social security or Tier 1 RRTA tax withholding,

from having 2 or more employers, you cannot file

1040EZ. You must file Form 1040 (PDF) or Form

1040A (PDF). To claim a refund of the Tier 2

RRTA tax, use Form 843 (PDF). If you are filing

a joint return, you cannot add any social

security or RRTA tax withheld from your spouse's

income to the amount withheld from your income.

You must figure the credit separately for both

you and your spouse to determine if either of

you had excess withholding.

For details, including how

to compute the amount of excess credit, refer to

Publication 505, Tax Withholding and Estimated

Tax.

To clarify: The "Excess Social Security and Tier 1

RRTA Tax Withheld" line on a 1040-- and "Form 843"--

are only for the use of those who DID receive "wages",

but had the FICA or Tier 1 RRTA sur-tax applied to

more of those "wages" than it should have been.

The sur-tax only applies to "wages" up to a certain

amount (currently $94,200). Those who had the

sur-tax applied to "wage" receipts above that amount

can use the "Excess Social Security and Tier 1 RRTA

Tax Withheld" line to claim a refund of that excess

amount withheld.

Those who have received no "wages"

CANNOT have "Excess Social Security Tax Withheld".

They can only have "Improper Social Security Tax

Withheld", and the proper way to reclaim it is by

combining it with normal federal income tax withheld

for one big figure on the appropriate line of a

1040.

See this for more.

|

A Thumbnail

Sketch Of The "Income" Tax Reporting And

Determination Process

A helpful summary of certain core "income" tax

dynamics

At the close of the reporting period (December 31st,

in most cases), payers considering themselves

obliged to issue taxable activity reports create and

execute one or more of the various "information

return" reports (W-2s, 1099s and K-1s, mostly),

sending one copy to federal, state and/or local tax

agencies, and one copy to the person about whom the

document makes its allegations.

Having thus been put on notice that allegations of

having received "income" have been reported to the

government(s) to whom any resulting tax would be

owed, the reportee either:

A. Lets the allegations go without response--

thus inviting the tax agency (we'll just focus

on the federal system, now) to:

-

presume them correct and true;

-

create a "SFR" "module" in order to

calculate the resulting tax liability

(without going into the legitimacy of doing

so in any particular case-- if no response

has been made to "income" allegations, a

door has been left pretty wide open for all

manner of presumptions about the legal

status of the reportee); and to

-

claim ownership of any withheld or

paid in amounts up to that calculated

liability, and/or (eventually) issue an

appropriate "Notice of Deficiency" for any

outstanding balance.

(NOTE: The agency is also thus invited to impose

available statutory sanctions, such as a

"failure to file" penalty, for instance.

This is because the requirement to file-- which

generally arises upon receipt of a threshold

amount of "income"-- and jurisdiction for the

imposition of sanctions have been presumptively

established by the allegations of the taxable

activity report and the failure of the reportee

to rebut them after being put on notice.)

or

B. Responds to the allegations by filing a valid

(that is, accurate, honest, and self-consistent)

return which either:

1. Acknowledges the reported taxable

activity ("income"), claims appropriate

deductions, credits, exemptions etc.,

calculates the resulting tax liability and

self-assesses,

or

2. Corrects or rebuts the reported "income"

amount(s), claims appropriate deductions,

credits, exemptions etc. (if applicable and

relevant), calculates the resulting tax

liability and self-assesses (very possibly

resulting in an assessed liability of $0.00

and a claim for the return of everything

withheld or paid-in).

(NOTE: Returns rebutting allegations of the

receipt of "wages" and/or "trade or

business"-generated "income" simultaneously

rebut jurisdictional presumptions which could

otherwise be supported by those allegations.)

In the case of B(1) or B(2), the IRS can then:

a. Issue a refund check or credit (if

the self-assessed amount is less than

the amount withheld, paid in, carried

forward, or otherwise available for

crediting for that period-- thus

resulting in an "overpayment");

b. Bill the filer for any balance due if

the amount assessed on the return is

more than the amount withheld, paid in,

carried forward, or otherwise available

for crediting for that period;

or

c. Make a determination that the amount

self-assessed is deficient and issue a

"Notice of Deficiency"-- but only on the

basis of the rate of tax having been

incorrectly applied to the amount of

"income" shown on the return (through

math and/or deduction/exemption/credit

reduction errors).

It will be noted that each of these latter IRS

response options are confined to calculations based

on the amount of "income" reported on the return.

When a return has indeed been filed, the agency has

no authority to do otherwise. This is why when

it wishes to thwart an educated American (which is

to say, when it wishes to evade the tax laws and the

required issuance of properly-claimed refunds), the

IRS will try to deny the relevant return was ever

filed.

Toward that end, the agency has actually gone so far

as to deny ever having received the returns of some

educated filers whose returns made claims the agency

did not wish to honor-- an, "Our junk-yard dog

must've eaten your tax return!" routine.

This only delays the inevitable for a brief time, of

course, while the filer walks a copy in to the local

office and personally oversees having it stamped as

received, or otherwise secures incontrovertible

evidence of the agency receiving the filing.

Thus, alternative ploys are becoming more common

when the IRS wishes to evade the law. One is a

simple declaration that the return is "frivolous"

(under the statutory definition at 26 USC 6702-- a

status which, when accurate, means the return can be

treated as though never filed, according to current

doctrine), in the hope that the filer will back down

in confusion and fear. (Click

here for more about this revealing ploy, which

would obviously never be attempted if the law

provided for any other means of defeating a claim,

and

here for a series of case-studies of CtC

Warriors who have dealt with this, and other

tax-agency ploys.) Then the agency will follow

up with with the steps outlined earlier in section

"A."

Another is to invite the filer to abandon his

testimony, by proposing alternative numbers on a

convenient form which the filer can sign under

penalty of perjury and thus adopt as a modification

of his previously-filed return-- as though what had

been filed must simply have been a big mistake, from

which the filer will surely back down (in confusion

and fear).

CtC-educated Americans do not back down in

confusion and fear, of course...

|

|

Q.

Does it matter if

multiple returns are sent to a tax agency at the same

time (or in the same envelope), as opposed to one at a

time (either by mailing date or packaging)?

A. It is hard to imagine why any such detail would

make a bit of difference, absent some published request

by the agency that things be done in a particular way

for bureaucratic processing purposes (personally, I've

never seen an official request in this regard, although

I've also never looked...). Best way to find out,

if this is really a concern, is to call the relevant

agency and ask, I would think.

That said, I understand that this question reflects the notion that one should strive to

avoid "standing out", presumably based on the view that

tax agencies are unscrupulous and will target for

harassment and resistance even perfectly proper filings

and claims that come to their attention. But this notion

itself reflects a misunderstanding of just

what exercising one's right to introduce one's testimony

into the record (or simply claim a return of one's

property)-- and, more broadly, standing up for the rule

of law-- is all about. Subterfuge, or the wish to be

"off the radar screen", has no place in the upholding of

the law. Tricks and shadows are for those doing

wrong, not for those doing right. (See

this for some

related material.)

|

|

Q. I've read through your book

and searched the website for information on how to

possibly report capital gains and dividends from

non-national banks. My first thought is capital gains

are only paid by taxpayers not non-taxpayers but I

really don't know.

A. In order to qualify as "income", any gain,

however labeled, must be of the same general legal

character as anything else that so qualifies. That

is, in order to qualify as "income" any gain must be a

consequence of the (profitable) benefit

of the exercise of

a federal privilege, power or

property (which may, of course, be an "exercise by

proxy" in the form of an investment in an entity which

is doing the "exercising" directly).

By the same token, allegations (or actual

receipt) of "capital gains" can and should be addressed

in exactly the same way as any other allegation (or

actual receipt) of "income", however labeled. Generally,

the appropriate model will be how one would handle what

would be reported or alleged by way of a "1099-MISC".

BTW, get clear on this important cognitive

nugget: anyone can potentially be a

"taxpayer". It is not the character of the actor

that makes gains taxable (even though because of their

nature some actor's gains will always be of a taxable

character), it is the character of the gains that makes

an actor into a "taxpayer" (insofar as-- and only

insofar as-- those particular gains are concerned).

|

|

Q. Am I stuck in an "administrative

proceeding" with the tax agency once I file a return?

A. Quite the contrary. Filing an accurate,

proper return on which less than the exemption amount of

"income" is declared establishes that one IS NOT in an

administrative proceeding with the relevant tax agency.

This is why tax agencies try so hard to induce everyone

to let the agency disregard the filed return, using any

means necessary from elaborate efforts to suggest the

returns are somehow defective (and that the agency is

authorized to make such determinations unilaterally!) to

the frankly comical claim that, "The return must have

gotten lost in the mail, Mr. Smith!" (See the 'Every

Which Way But Loose' collection for more on this.)

On the other hand, those who declare having received

more than the exemption amount of "income" on a return--

or don't file, and allow "information return"

allegations of having received more than the exemption

amount of "income" to prevail by default-- ARE stuck in

such a proceeding. These unfortunates have become

"taxpayers" subject to such proceedings due to (and to

the extent of) those declarations or unanswered

allegations.

|

|

Q. What about getting loans?

Lenders usually ask to see tax returns. Won't

accurate tax returns which show no (or little) "income"

make it impossible to get a loan?

A. Actually, lenders and others who provide

earnings-related financial services don't have any

interest in how much "income" anyone does or doesn't

make, generally (although there may be some federal

financial service entities specifically providing

"income"-related services that would be exceptions to

this, I suppose). Financial services folks are

really only interested in how much money one makes,

because that's what matters where one's ability to repay

a loan, or one's qualification for aid, or whatever, is

concerned.

A number of CtC Warriors have had this issue arise.

They have found that the folks with whom they are

dealing are perfectly happy to accept alternatives to

tax returns for documentation of earnings, such as pay

stubs, affidavits, bank statements and so forth.

In the face of truly mindless resistance to

alternatives one might consider submitting complete tax

returns, but particularly including rebuttal instruments

such as forms 4852 and rebuttals to 1099s, K-1s and so

forth which would help make clear that the 1040 form is

not a declaration of having not received money, but only

of having not received "income". W-2s could also be

presented, with a notation to the effect that while the

inherent characterization of the payments reported on

the forms as being from taxable activities is disputed

and rebutted, the forms serve as evidence of the payee's

receipt of money in the amounts shown.

|

|

Q. Is there any need or

virtue to including legal arguments in a filing

supporting or justifying what is being reported?

A. In a word, no. Once a testimonial

declaration as to the factual matters with which the

filing is concerned is made (by way of the return) and

appropriate testimonial declarations in rebuttal of any

allegations that amounts were received during the

relevant period as a consequence of engaging in a

taxable activity (by way of affidavits in response to

"information returns", such as Forms 4852, or corrective

responses to 1099s, etc.), the tax agencies are required

as a matter of law to accept that testimony as

definitive and final.

Further, even if the

agencies were NOT required to accept the filer's

testimony, a tax agency/government that wishes to assert

a competing claim to what has been established by the

filer's declarations would bear every burden of proving

its claim.

Unless someone has already conceded the point in his or

her filed return, or given it up by default through

non-filing, the burden of proving that IT has a claim to

withheld money is ALWAYS on the government in any

dispute situation. The return will have formally

asserted the filer's continuing ownership and right to

possess that property:

�Even if you do not otherwise have to file a

return, you should file one to get a refund of any

Federal income tax withheld.�

From the instructions for the 2002 Form 1040

***

26 CFR 301.6402-3

Special Rules applicable to income tax

(a) In the case of

a claim for credit or refund filed after June 30,

1976--

(1) In general, in the case of an overpayment of

income taxes, a claim for credit or refund of such

overpayment shall be made on the appropriate income

tax return.

...

(5) A properly executed individual, fiduciary, or

corporation original income tax return or an amended

return (on 1040X or 1120X if applicable) shall

constitute a claim for refund or credit within the

meaning of section 6402 and section 6511 for the

amount of the overpayment disclosed by such return

(or amended return).

***

Senator Clark: "Of course, you withhold not

only from taxpayers but nontaxpayers."

Mr. Hardy: "Yes."

...

Senator Danaher: "I have only one other thought

on that point. In the event of withholding from the

owner of stock and no taxes due ultimately, where

does he get his refund?" Mr. Friedman:

"You're thinking of a corporation

or an individual?"

Senator Danaher: "I am talking about an

individual."

Mr. Friedman: "An individual will file an income

tax return, and that income tax return will

constitute an automatic claim for refund."

Excerpted from a Withholding Tax hearing

on August 21 and 22, 1942 before a subcommittee of the

Committee on Finance, United States Senate, during the

77th Congress, Second Session, on data relative to

withholding provisions of the 1942 Revenue Act. Missouri

Democratic Senator Bennett Clark, Connecticut Republican

Senator John A. Danaher and testifying witnesses Charles

O. Hardy of the Brookings Institution and Milton

Friedman of the Treasury Department Division of Tax

Research.

The filer does not have to prove his ownership and right

to that property-- it never stops belonging to him

unless and until a competing claim could be, and is,

proven both: 1.) to be possible (that is, until it is

proven that he actually engaged in a relevant taxable

activity) and 2.) to have been asserted in a legally

meaningful way (that is, until it is proven that a valid

assertion of the government's contrary alleged claim can be, and

has been, made in a legally meaningful way). See

this for more on "asserted in a legally meaningful

way".

Further, this same dynamic applies anytime a tax agency

suggests that it gets to assume ownership of anyone's

property (either by taking that property or by keeping

it) in the face of a proper assertion of ownership and

claim for refund by the annual filer. "We

changed your account [to our benefit]...", for

instance, doesn't mean anything unless preceded by,

"We proved that you did something making you beholden to

us for $x.xx, that we have the authority to assert our

claim despite your relevant filed return(s) and self

assessment(s), and that we did, in fact assert that

claim in a legally meaningful manner." Otherwise, it's really just, "We're implying that we

have some god-like authority to assume ownership of

whatever we wish, and we hope you've been sufficiently

brow-beaten and confused by the life-long conditioning

to which we have subjected you to imagine that this

could be true..."

(NOTE: See 'About 1040s And Claiming Refunds' in

CtC for more on this subject.)

|

|

Q. Does filling out a W-4 make one

into an "employee", and one's pay into "wages", or

amount to a voluntary election to be treated as an

"employee" (and having one's pay treated as "wages")?

A. The completion and submission of a W-4 doesn't

make someone not engaging in taxable activities into

someone who is (nor does it constitute an election to be

so treated as though one were engaged in such

activities). After all, filling out a W-4 doesn't

constitute the completion of a federally-connected civil

service application or an oath of office, or becoming an

officer of a federal or federally-controlled

corporation...

Thus, for one who is not actually an "employee" the

completion of the form must be presumed to be entirely

prospective in nature, providing in advance for the

theoretical possibility (however remote) that one's

relationship with the company to which one presents the

form might somehow become that of "employer" and

"employee" at some unknown point in the future (while

otherwise being legally irrelevant). Whether or

not such a theoretically-possible change actually takes

place at any point is reflected in the content of one's

filing concerning each past year.

That said, the submission of a W-4 without a qualifying

declaration COULD serve to support inaccurate

presumptions about the nature of one's activities.

See 'W-4s- The Blind Leading The Blind...' in CtC and

what you find here for

more on this.

|

|

Q.

Does using Federal Reserve Notes (FRNs) make an activity

taxable?

A. In a word, no.

CREATING FRNs might be the exercise of a federal

privilege or power, but using them certainly is not, any

more than using the interstate highway system or getting

scanned by the TSA at an airport are taxable activities,

or make anything you do on your trip a "taxable

activity". No such things are specified as taxable in

any law. Nor could they be, as each would make the

income tax an improper capitation in that any of these

(and especially the "using FRNs" one) would effectively

lay the tax on all economic activity.

Further, "gain" is an integral requirement of "taxable"

and there is no "gain" from the use of FRNs because of

some speial characteristic of the notes, whether

accepting them or paying with them (other than as their

creator). If anything, someone being paid FRNs is

thereby inherently losing value, due to the inflation to

which the notes are inherently vulnerable.

On the other hand, being paid with FRNs IS a measure of

economic activity in the normal sense of the term and is

a receipt of value, however much one might feel their

issuance to be Constitutionally invalid. Whatever else

may be said about FRNs, they ARE claims against the

assets of their issuer, as is plainly declared in 12 USC

� 411:

"Federal reserve notes, to be issued at the

discretion of the Board of Governors of the Federal

Reserve System for the purpose of making advances to

Federal reserve banks through the Federal reserve

agents as hereinafter set forth and for no other

purpose, are authorized. The said notes shall be

obligations of the United States and shall be

receivable by all national and member banks and

Federal reserve banks and for all taxes, customs,

and other public dues. They shall be redeemed in

lawful money on demand at the Treasury Department of

the United States, in the city of Washington,

District of Columbia, or at any Federal Reserve

bank."

Clearly, receiving FRNs is no different from receiving

any other medium of exchange in any sense relevant to

the tax.

Further still, the law specifically says that what

someone engaging in taxable activity gets paid in

doesn't matter. It isn't the being paid, or what one is

being paid with that matters, it's what one did

for which one is being paid

that matters.

See 'A "Wage" By Any Other Name Is Taxed The Same' in 'Was

Grandpa Really a Moron?' for more about this; also

see the definition of "gross income" as interpreted by

the Treasury Department at 26 CFR � 1.61-1(a)

"(a) General definition. Gross income means all

income from whatever source derived, unless excluded

by law. Gross income includes income

realized in any form, whether in money, property, or

services. Income may be realized, therefore, in the

form of services, meals, accommodations, stock, or

other property, as well as in cash."

(emphasis added);

and the definition of

"wages" at 3401(a):

"(a) Wages

For purposes of this chapter, the term �wages� means

all remuneration (other than fees paid to a public

official) for services performed by an employee for

his employer, including the cash value of all

remuneration (including benefits) paid in

any medium other than cash..." (emphasis

added).

When one combines this with the fact that

other portions of law specifically provide that some

payments to "employees" for services performed for an

"employer" DON'T qualify as 'wages" and are NOT subject

to the tax, and do so without a qualifying specification

negating these exceptions of taxable status if payment

is made in FRNs, it is clear that not only does no

provision of law support the proposition that use of

FRNs is taxable, but the structure of the law positively

contradicts this notion.

|

|

Q. Is it a privileged, taxable

activity to act economically as a "licensed this or

that"?

A. A license is permission to engage

in the licensed activities for, or with, the licensor.

That is, if one acquires a license from a state to

perform some activity (such as a plumber's license) the

only privilege that can be being conveyed by the license

is that of performing the activity for the state. After

all, it's obvious that anyone has a right to sell

plumbing services to anyone else generally, and doing so

isn't exercising any privilege.

Consequently, activity performed for the licensing

entity is potentially taxable by that entity as the

exercise of privilege (though it may or may not actually

be taxed-- for instance, it may be that the only actual

tax applied in connection with licenses issued by one of

the several states may be the fees associated with

getting and maintaining the license). At the same time,

the same activity performed by the same person elsewhere

would remain just an activity of common right, not

subject to that privilege tax as such. Even performing

the activity for someone who insisted on the performer

having such a license in order to be hired would not

make that performance into the conduct of a privilege

granted by the licensing entity.

Sensibly or not, such insistence is common, because

licenses have historically been seen as implying

superior skill or as evidence that the licensee has met

some tested level of quality. Those able to do so have

always advertised their positions as "dressmaker to the

Queen" or "licensed to argue cases before the King's

bar", figuring it gave them a leg-up on the competition

in marketing themselves to others. The notion, I

imagine, is the sub-textual suggestion that "the King"

or "the Queen" can afford, or will always insist upon,

the best, so someone to whom they've granted license to

do business with the apparatus of the state must really

be good. Those seeking services often buy into these

notions, and insist that their service-providers be able

to exhibit licenses. But the fact that someone is

"licensed" to do privileged work doesn't make work one

has every common right to do into something taxable by

the licensor.

By the way, a significant legal doctrine rears its head

in connection with licensure. As observed by a court in

an 1869 ruling concerning a challenge in part to the

Constitutionality of the power of the government under

section 49 of the revenue act of 1868 to "examine all

persons, books, papers, accounts and premises", and to

compel persons to appear, and to produce books and

records, in order to ascertain the correctness of a

return (In re Meador, 16 F. Cas. 1294 (ND Ga.

1869)):

And here a thought suggests itself. As the

Meadors, subsequently to the passage of this

act of July 20, 1868, applied for and

obtained from the government a license or

permit to deal in manufactured tobacco,

snuff and cigars, I am inclined to be of the

opinion that they are, by this their own

voluntary act, precluded from assailing the

constitutionality of this law, or otherwise

controverting it. For the granting of a

license or permit-- the yielding of a

particular privilege-- and its acceptance by

the Meadors, was a contract, in which it was

implied that the provisions of the statute

which governed, or in any way affected their

business, and all other statutes previously

passed, which were in pari materia

with those provisions, should be recognized

and obeyed by them. When the Meadors sought

and accepted the privilege, the law was

before them. And can they now impugn its

constitutionality or refuse to obey its

provisions and stipulations, and so exempt

themselves from the consequences of their

own acts?

Of course, even under this doctrine the

government actions to which the licensee could be said

to have agreed by implicit contract must be confined to

those concerning the exercise of the privilege granted,

not any and all activity of the licensee period. That

is, the government can (under this doctrine) freely

examine the books of the licensee in which his sales,

etc., under the permissions of the license are made

(which is to say, those to the licensing entity), but

not his sales to the

general public for which no license is needed (even

though what is being sold is exactly the same as what he

is licensed to sell to the government).

In fact, in the later case of

Stanwood v.

Green, 1870 U.S. Dist. Lexis 279 (1870) which

dealt with the same subject, the court explicitly

draws the distinction between the two classes of

otherwise identical activities, acknowledging that a

target of an examination summons need only produce

that portion of his business records concerned with

his taxable activities (see the discussion of

this ruling in the "NOTES" section of

this page). But no one should be surprised if a

pretext will be seen by virtue of a license under

which the government claims the need and right to

examine ALL business activities concerning the

object of the license anyway, in order to ensure

that the taxable portion of these activities are

accurately reported...

|

|

Q. Are activities as a public school

teacher subject to the tax?

A. If a public school teacher's activities are as a

federal school teacher, such as those discussed

here, they would be potentially subject to the

"income tax" (I say "potentially" because not all

"income" is actually always subjected to the tax, even

though it qualifies). The personal services of public

school teachers rendered in the capacity of "an officer

or employee of a State, or any political subdivision

thereof, or any agency or instrumentality of the

foregoing," are also included-- where "State" is defined

as in the discussion of the Public Salary Tax Act of

1939 on pp. 70-72 of CtC. By the same token, this would

exclude public school teachers who are NOT of these

varieties (which is to say, any working for a

union-state school-district).

The parameters are not expanded or affected by federal

grants or other federal foot-prints littering the halls

of public schools not meeting the criteria outlined

above. Just as the benefit of federal privilege

exercised by an otherwise private business makes the

business's profits potentially taxable, but not the

earnings of the workforce-- even though possibly being

paid straight out of money secured from the feds, the

institutions (such as the school districts or schools

themselves) which receive education-related grants and

other benefits might themselves be subject to

obligations and liabilities thereby (and not only

tax-related obligations and liabilities), but this

doesn't reach further to penalize or encumber the

work-force. THEIR relations are just with the

institution, not the institution with which their

institution has relations.

|

|

Q. What About Bitcoin?

A. THERE HAS BEEN A FLURRY OF WORRY and

fuss over recent IRS efforts to secure information

on bitcoin transactors. The anxiety is misplaced.

Let me say first that there is nothing

inherently taxable about using or receiving bitcoin.

It's just a medium of exchange like any other. There

is no tax on exchanges per se, nor on profits, gains

or receipts, per se.

By the same token, however, there is

a tax-- measurable by the value of bitcoin

received-- for doing taxable things resulting in

those receipts. That is, not all things done for

which bitcoin might be received are taxable, but the

receipt of bitcoin is relevant to the tax when

received for doing taxable things.

THE BOTTOM LINE IS that concern about

IRS prying into records of bitcoin transactions is

misdirected. The concern should be at the prying

itself, without regard to the bitcoin element.

Unless it has been previously

established that a taxable activity has been

conducted, the IRS has no valid interest in any

transaction. Thus, a blanket demand for information

on all transactions is an offensive, possibly 4th

amendment-violating intrusion.

AT THE SAME TIME, anyone and everyone

engaging in bitcoin transactions and troubled by

these bureaucratic intrusions MUST BECOME

CtC-EDUCATED. That and that alone will protect

from all the practical ill-effects of such

intrusions (which routinely happen in other venues,

such as conventional banking, anyway).

Only those ignorant of the hidden

truths about the income tax have reason to fear

information falling into the hands of the IRS. So,

keep on keeping crypto. Just

get educated about the tax, too.

|

Frequently Asked Questions Page 1

|