|

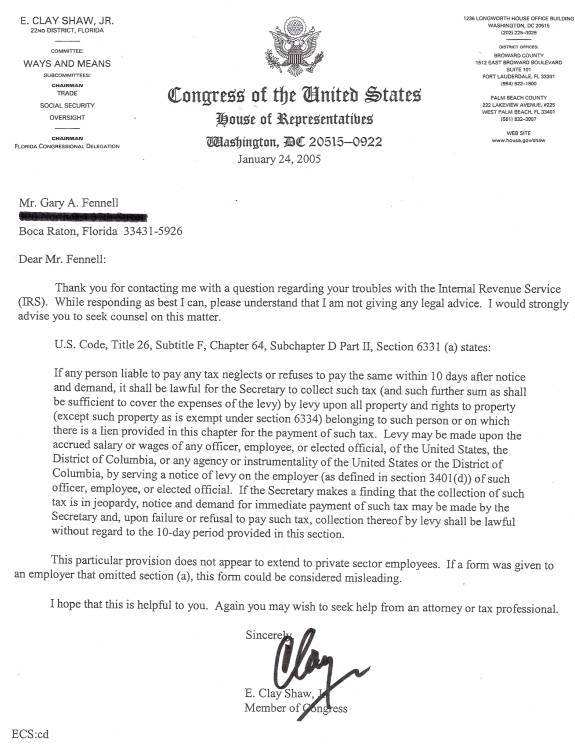

Regarding a "Notice Of Levy" Anyone whose employer is sent a "Form 668-W Notice of Levy on Wages, Salaries, and Other Income", a standard tactic used to co-opt third parties into doing for the IRS what it can't do for itself, (and entirely at that third party's risk, by the way), will take great interest in noting that the IRC excerpts thoughtfully provided on the back of the form, from section 6331 of the code, leave out the first paragraph of that section, paragraph (a), and begin with paragraph (b). The missing section is as follows (with emphasis added): SECTION 6331. Levy and distraint. (a) Authority of Secretary--If any person liable to pay any tax neglects or refuses to pay the same within 10 days after notice and demand, it shall be lawful for the Secretary to collect such tax (and further sum as shall be sufficient to cover the expenses of the levy) by levy upon all property and rights to property (except such property as is exempt under section 6334) belonging to such person or on which there is a lien provided in this chapter for the payment of such tax. Levy may be made upon the accrued salary or wages of any officer, employee, or elected official, of the United States, the District of Columbia, or any agency or instrumentality of the United States or the District of Columbia, by serving a notice of levy on the employer (as defined in section 3401(d)) of such officer, employee, or elected official. If the Secretary makes a finding that the collection of such tax is in jeopardy, notice and demand for immediate payment of such tax may be made by the Secretary and, upon failure or refusal to pay such tax, collection thereof by levy shall be lawful without regard to the 10-day period provided in this section. Lacking this paragraph, an business receiving one of these invitations to conspiracy might not realize that they are taking responsibility for establishing that the proposed target of the "notice of levy" is both a covered person subject to this statutory protocol, as defined in paragraph (a) above; and is liable to pay a tax. (A mere declaration that someone owes money has no legal standing, and particularly not in the face of that someone's disagreement). Acting in error on these points potentially creates several serious legal liabilities of both a criminal and civil nature for the company. This letter written by Congressman Dennis Hertel when he was representing the 14th District of Michigan is worth a look:

A similar, and more recent statement by another member of congress A more comprehensive discussion of this subterfuge can be seen here.

|

{kind=link}